23rd March 2026BY Nihang Law

Can I Pay My Parent’s Bills in Ontario If They Become Incapable? How a Power of Attorney for Property Works

In Ontario, the document most people need for future financial incapacity planning is a Continuing Power of Attorney for Property. It can authorize a trusted person to manage banking, bills, investments, debts, and even real estate, but not to make a will. It may take effect right away or only when a stated condition is met, depending on how it is drafted. It is not filed in a general government registry, and it stops on the grantor’s death.

Last Updated: March 2026

A lot of Ontario families discover the problem too late. A child may assume they can “just call the bank,” only to learn that being next of kin does not automatically give full authority over a living adult’s finances. Situations like this are one reason many families review their broader estate planning in Ontario before a crisis arises.

If there is no valid continuing power of attorney and the person is already incapable, the file can shift into statutory guardianship or a court-based guardianship process, with the Public Guardian and Trustee potentially involved. That usually means more delay, more paperwork, and less control over who manages the property.

Legal Disclaimer: This article is general legal information for Ontario readers. It is not legal advice. Powers of attorney are highly fact-specific, and the right next step may depend on capacity, the wording of the document, the assets involved, and whether a bank, title office, or court process is already involved.

Quick Start: Pick Your Path

You are planning ahead while still capable:

- Prepare a continuing power of attorney for property before a crisis arises.

You are the named attorney and need to use it now:

- Check whether it is effective immediately or only on incapacity, then gather the original or a notarized copy and expect institution-specific review.

Your loved one is already incapable and no valid document exists:

- Assess whether statutory guardianship or a court guardianship application is now required.

A house sale, refinance, or transfer is involved:

- Have the document reviewed carefully because real estate use of powers of attorney gets extra scrutiny in Ontario.

What is a Power of Attorney for Property in Ontario?

Which Kind Matters When Incapacity is the Concern?

A continuing power of attorney for property is the Ontario document designed for financial incapacity planning. It lets a named attorney manage property and finances even if the grantor later becomes mentally incapable. A general or non-continuing power can help with temporary financial tasks, but it does not survive incapacity.

Ontario recognizes more than one kind of power of attorney. The one that matters most for this scenario is the Continuing Power of Attorney for Property. It covers financial affairs and survives incapacity. A general or non-continuing power of attorney for property may be useful if someone is travelling, ill, or unavailable, but it stops being effective if the person becomes mentally incapable. A power of attorney for personal care is different again: it deals with health and personal care decisions, not money or property.

Document | What it Covers | Does it Continue After Incapacity? | Common Use | Main Risk If Misunderstood |

Continuing Power of Attorney for Property | Money, assets, bills, banking, investments, real estate | Yes | Incapacity planning | People may wrongly assume it also covers health decisions |

General / Non-Continuing Power of Attorney for Property | Financial tasks only | No | Temporary absence or limited delegation | It stops being effective if the person becomes incapable |

Power of Attorney for Personal Care | Health, housing, care decisions | Different legal rules | Medical and care planning | It does not authorize management of money or property |

The table reflects Ontario’s basic distinction between continuing property authority, non-continuing financial authority, and personal care authority.

Nihang Law Insight

In practice, one of the most common problems is not the absence of a document, but the wrong document. Families often bring in a personal care POA, a foreign POA, or a short-form banking authorization and assume it will cover a house sale, investment account, or urgent bill payments. Often, it does not.

When Does a Continuing Power of Attorney for Property in Ontario Start?

What Can the Attorney Actually Do?

A continuing power of attorney for property in Ontario can start immediately or on a later date or contingency written into the document. Unless the document limits the authority, the attorney can generally do anything with respect to property that the grantor could do if capable, except make a will.

Can Usually Do | Caution / Conditions | Cannot Do |

Pay bills and | Banks may | Make or |

Deposit | The POA may | Make |

Manage | The attorney | Keep acting |

Deal with | A document | Use the role |

Take | Gifts, loans | Ignore the |

Ontario’s statute allows a continuing power of attorney to be effective on a specified date or when a specified contingency happens. If the document says it becomes effective on incapacity but does not explain how incapacity is to be determined, the Act supplies a mechanism, including notice from an assessor in the prescribed form or notice of a certificate of incapacity under the Mental Health Act.

The attorney’s authority can be broad. Under the Substitute Decisions Act, 1992, the attorney may do anything in respect of property that the grantor could do if capable, except make a will. In real life, that may include paying bills, dealing with investments, collecting debts, buying goods and services, starting or defending lawsuits with financial implications, and maintaining or selling a home or vehicle, subject to any restrictions written into the document. In many files, that practical authority also raises questions about digital assets and online accounts, especially where banking, email access, or record-keeping overlap. If more than one attorney is appointed, they act jointly unless the document says otherwise.

Who Can Make It, Who Can Witness It, and What Makes It Invalid?

In Ontario, the grantor must be at least 18 and capable of giving a continuing power of attorney for property. The document must be signed in front of two witnesses, and several categories of people are disqualified from witnessing, including the attorney, the grantor’s spouse or partner, and the grantor’s child.

Ontario does not require a special form, but the document must either be called a continuing power of attorney for property or clearly say that the authority continues if the grantor becomes mentally incapable. The grantor must understand the nature of their property, obligations to dependants, the scope of the attorney’s authority, the duty to account, the ability to revoke while capable, the risk of poor management, and the possibility of misuse.

The witnessing rules matter. The attorney, the attorney’s spouse or partner, the grantor’s spouse or partner, the grantor’s child, a person under 18, and certain persons under guardianship cannot witness. If the document does not comply with the witnessing requirements, it is generally ineffective, although the court can declare it effective in an appropriate case if that is in the interests of the grantor or dependants.

Nihang Law Insight

This is where “do-it-yourself” documents most often break down. A family may feel relieved that something was signed, only to learn later that one witness was disqualified, the document never said it was continuing, or the incapacity trigger was drafted so vaguely that the bank will not act on it without further proof.

What Duties Does an Attorney for Property Owe, and Can They Pay Themselves?

An attorney for property is not just a helper. Once the grantor is incapable, the role carries fiduciary duties, record-keeping obligations, and rules about expenditures and compensation. The attorney must act diligently, honestly, in good faith, and for the incapable person’s benefit, while keeping proper accounts.

Under section 38 of the Substitute Decisions Act, many of the same rules that apply to guardians of property also apply to an attorney acting under a continuing power of attorney where the grantor is incapable or the attorney reasonably believes the grantor is incapable. That includes fiduciary duties, participation and consultation duties, and the obligation to keep accounts. The attorney must consider the person’s benefit, encourage participation to the extent possible, and keep records of transactions involving the property. When those duties are ignored, disputes over power of attorney abuse and estate litigation can follow.

The law also controls expenditures. Required spending is prioritized toward the incapable person’s support, education, and care, then dependants, then other legal obligations. Gifts, loans to relatives or friends, and charitable gifts are more restricted and usually depend on past intention, the person’s present wishes, and financial sufficiency.

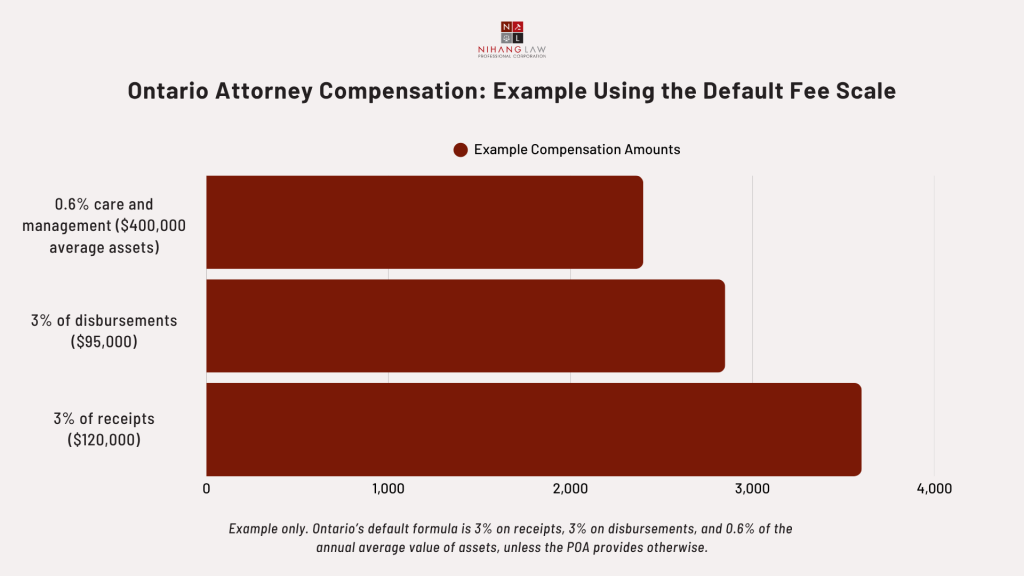

Compensation is possible, but not automatic in every practical sense. The statute says an attorney under a continuing power of attorney may take compensation according to the prescribed fee scale, unless the document changes that arrangement. Ontario’s regulation sets the usual scale at 3% on capital and income receipts, 3% on capital and income disbursements, and 3/5 of 1% of the annual average value of the assets as a care and management fee. The court may order a passing of accounts, and compensation can be reviewed there.

Figure 1: How Ontario Attorney Compensation Works: Example Using the Default Fee Scale

What Happens If the Person is Already Incapable and There is No Valid Power of Attorney?

If there is no valid continuing power of attorney and the person is already incapable of managing property, the family may need a statutory guardianship or court guardianship route. In some situations, the Public Guardian and Trustee becomes the statutory guardian of property first, and a relative or spouse later applies to replace it.

Situation | Who acts first? | Possible next step | Main downside |

Valid continuing POA already exists | Named attorney | Use POA, subject to document terms and institution review | Delay if the document is unclear or not accepted right away |

No valid POA and incapacity is found | Public Guardian and Trustee may become statutory guardian of property | Eligible person may apply to replace the PGT | Less family control at the outset |

PGT refuses replacement application | PGT gives written reasons | Dispute may go to court | More time and cost |

Ontario’s statute provides that when a certificate of incapacity is issued after a capacity assessment for this purpose and the Public Guardian and Trustee receives it, the Public Guardian and Trustee becomes the person’s statutory guardian of property. The incapable person must then be informed that this has happened and that they may apply to the Consent and Capacity Board for a review of the incapacity finding.

There is an important exception. If the person had already given a continuing power of attorney covering all of their property before the certificate of incapacity was issued, the statutory guardianship can be terminated once the Public Guardian and Trustee receives the required authenticated document, written undertaking, and identity proof. If there is no such full document, a spouse, relative, or qualifying trust corporation may apply to replace the Public Guardian and Trustee as statutory guardian, usually with a management plan.

Nihang Law Insight

For families, this is often the most stressful point: the person is already vulnerable, bills are due, and everyone assumes there is a quick fix. Sometimes there is. Sometimes there is not. Early legal review matters because the path changes completely depending on whether a valid continuing POA already exists.

Will Banks, Title Offices, and Third Parties Automatically Accept the Document?

Not always. A valid Ontario power of attorney may still be reviewed carefully by banks, lenders, and land registration professionals. Institutions may ask for the original or a notarized copy, may have internal review timelines, and may refuse to act until their procedural requirements are met.

The Office of the Public Guardian and Trustee explains that powers of attorney do not need to be registered in a general government registry and are not public records. But it also notes that a person asked to recognize the document may require a notarized copy or the opportunity to inspect the original before dealing with the attorney. Federally, the Financial Consumer Agency of Canada says member banks must provide information about their minimum POA requirements, review needs, expected review time, and complaint options, and must acknowledge that customers may use POA forms from sources other than the bank itself.

Real estate files involve extra caution. Ontario land registration material states that a document signed under a power of attorney generally cannot be registered unless the power of attorney itself is registered at or before registration. The Law Society of Ontario also warns that powers of attorney have been used in real estate fraud and says lawyers should treat their use as the exception rather than the rule and carefully scrutinize the authority.

What Does the Step-By-Step Roadmap Look Like in Ontario?

The roadmap depends on whether a valid continuing power of attorney already exists. The practical sequence is usually: find the document, confirm whether it is effective, satisfy bank or title-office proof requirements, set up proper accounting, and get legal help quickly if the document is missing, defective, or disputed.

1. Locate the original document and read the exact wording.

Confirm that it is truly a continuing power of attorney for property and check for limits, co-attorney rules, and substitute-attorney clauses.

2. Confirm whether it is already effective.

If the document postpones effectiveness until incapacity, determine whether it sets out its own proof method or whether the statutory assessment route applies.

3. Prepare for institution review.

Banks may want originals, notarized copies, identification, and time to review the authority.

4. Start a clean accounting system immediately.

Keep separate records of receipts, disbursements, investments, liabilities, compensation, and supporting documents.

5. Review real estate risk early.

If a sale, refinance, or registration is involved, do not assume the document will be accepted without advance review.

6. If no valid POA exists, pivot fast.

Assess whether statutory guardianship, replacement of the Public Guardian and Trustee, or a court guardianship application is now required.

What Mistakes Do People Commonly Make?

Most Ontario POA problems come from timing, drafting, or record-keeping mistakes rather than from the idea of the document itself. Common errors include these:

- Choosing a non-continuing financial POA when long-term incapacity planning was the real goal.

- Using disqualified witnesses or failing to meet two-witness execution rules.

- Assuming the attorney can make health decisions, change a will, or keep acting after death.

- Waiting until incapacity is already obvious, when the person may no longer have capacity to sign a new document.

- Treating family status as automatic legal authority over a living adult’s finances.

- Failing to keep receipts, ledgers, and compensation calculations from day one.

Frequently Asked Questions

Does a power of attorney for property let someone make medical decisions?

No. In Ontario, property and personal care are different legal roles. A power of attorney for property deals with financial and property matters. Health, treatment, housing, nutrition, and other personal care decisions fall under a different document: a power of attorney for personal care.

Does the attorney become the owner of the money or house?

No. The attorney gets authority to act on the grantor’s behalf; ownership does not transfer just because the document exists. The attorney is acting in a fiduciary role and must use the property for the grantor’s benefit, subject to the Act and the document’s limits.

Can the attorney sell the person’s home?

Often yes, if the continuing power of attorney gives broad property authority and does not restrict that power. But a real estate file may still require careful review by the lawyer, lender, title insurer, and land registration system because POA-based real estate transactions are treated cautiously in Ontario.

Do I have to register the power of attorney with the government?

Not generally. Ontario does not maintain a general public registry of powers of attorney, and registration is not required for ordinary validity. Land-related use is different, because a power of attorney may need registration in the land system before or at the same time as a document signed under it is registered.

Can two children act together as attorneys?

Yes. Ontario allows more than one attorney to be named. Unless the document says otherwise, they act jointly. That can be useful for checks and balances, but it can also create delay if one attorney is unavailable or the co-attorneys disagree.

Can the attorney resign?

Yes, but resignation is not just a private decision. If the attorney has already acted, the resignation is not effective until the required copies are delivered to the people listed in the statute, which may include the grantor, other attorneys, substitutes, and certain family members.

Can the attorney pay themselves?

Potentially, yes. Ontario law permits compensation under the prescribed fee scale unless the document changes or excludes that right. But compensation must be properly calculated and recorded, and it may later be reviewed on a passing of accounts.

What if the bank refuses to deal with the attorney?

Start by asking for the bank’s POA requirements, review process, and complaint route. FCAC says member banks must provide information about minimum requirements, review timing, and what happens if they refuse to act. In many cases, a lawyer’s review letter or better proof package helps move the file forward.

Reminder: A power of attorney only operates while the grantor is alive. It does not replace a will, and it does not let the attorney continue acting after death. That is one reason a POA should usually be reviewed alongside what happens if someone dies without a will in Ontario. At that point, estate authority is a different legal question. Once death occurs, the issue usually shifts from a POA to probate in Ontario and the role of the estate trustee.

Key Takeaways and How Nihang Law Can Help

A continuing power of attorney for property is one of the most important incapacity-planning documents in Ontario because it can keep bills paid, assets protected, and major financial decisions moving when someone can no longer manage their own affairs. But the details matter: the right kind of document, the right witnesses, the right trigger, the right record-keeping, and the right strategy if incapacity has already happened.

Where a family is dealing with an aging parent, cognitive decline, bank resistance, a disputed attorney, or a real estate transaction under a POA, the legal risk is rarely theoretical. A careful review early on may prevent a much more expensive guardianship, accounting, or litigation problem later. Nihang Law can help Ontario families review existing POAs, prepare new documents, assess attorney duties, and advise on guardianship or property-management issues when a valid POA is missing or challenged.

Sources & References

- Substitute Decisions Act, 1992 (CanLII)

- Powers of Attorney – Questions and Answers, Office of the Public Guardian and Trustee

- Duties and Powers of a Guardian of Property, Office of the Public Guardian and Trustee

- Make a power of attorney, Government of Ontario

- Guardianship, Government of Ontario

- O. Reg. 26/95: General

- O. Reg. 100/96: Accounts and Records of Attorneys and Guardians

- Continuing Power of Attorney for Property, CLEO

- How do I make a power of attorney?, CLEO

- Powers of Attorney: know your rights, Financial Consumer Agency of Canada

- Powers of attorney (for financial matters and property) and joint bank accounts, Government of Canada

- Guidelines on Powers of Attorney in Real Estate Transactions, Law Society of Ontario

- 83016 Power of Attorney, Ontario land registration

- Ontario population projections

- Population and demography statistics, Statistics Canada

- Dementia: Overview, Government of Canada

Thank you for reading this post, don't forget to subscribe!