3rd March 2026BY Qasim Nihang

Spousal Consent in Ontario: How a Non-Owner Spouse Can Block the Sale of a Matrimonial Home

Last Updated: March 2026

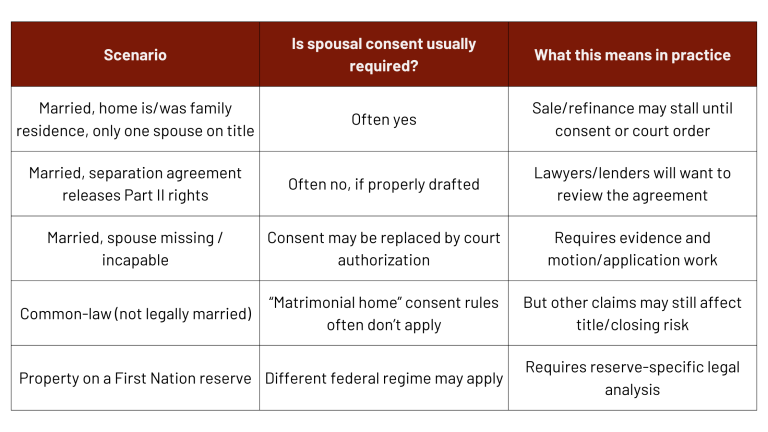

A married non-owner spouse can block a sale or refinance of a matrimonial home in Ontario because the Family Law Act generally prohibits selling or mortgaging that home without the other spouse’s written consent or a court order.

If the titled spouse tries to proceed anyway, the transaction may be set aside unless the buyer/lender qualifies as a good-faith party without notice.

If consent is being unreasonably withheld (or the spouse cannot be found/cannot consent), a court may authorize the transaction on conditions.

In a live deal, these issues often surface late, either during financing, lawyer due diligence, or immediately before closing. As such, early planning matters.

You accept an offer. You book movers. You’re counting on the sale proceeds to buy the next place, or pay off debt, or simply end a stressful chapter. Then your lawyer (or the lender) asks one question that freezes everything:

“Are you married, and is this a matrimonial home?”

If the answer is yes, the deal may not close without a signature from a spouse who isn’t even on title. That can feel shocking—especially when the relationship is strained, you’ve been separated for months, or the spouse moved out long ago. But Ontario’s rules are designed to prevent one spouse from quietly selling (or mortgaging) the family home and leaving the other spouse without housing leverage.

The good news: there are lawful ways to move forward. The bad news: you typically can’t “paper over” this in the last 48 hours before closing without cost, delay, or court involvement.

Legal Disclaimer: This article is general information about Ontario law, not legal advice. Every file turns on its facts. If you need advice for your situation, speak with a lawyer.

Quick Start: Pick Your Path

Seller on title (trying to sell or refinance)

- Confirm if you are legally married (not just common-law).

- Confirm if the property is (or was at separation) ordinarily occupied as a family residence.

- If yes, plan for spousal consent or a court order.

- If consent is refused: consider negotiated terms, temporary housing plan, or court relief.

Non-owner spouse (trying to protect housing rights)

- Confirm you are a married spouse under Ontario’s Family Law Act.

- Gather proof the home was a family residence at separation.

- Get legal advice before signing anything—consent can change leverage quickly.

Buyer (trying to avoid a closing disaster)

- Ask early whether the seller is married and whether the home is/was a matrimonial home.

- Ensure the seller’s lawyer provides proper spousal statements or confirmations (typical Ontario conveyancing practice relies on statutory statements).

- Be cautious with “no conditions” offers if occupancy history suggests family-law risk.

Realtor or lender (risk management)

- Flag spousal consent early—before listing strategy, staging spend, or underwriting.

When is a Property a “Matrimonial Home” in Ontario?

In Ontario, a matrimonial home is every property in which a spouse has an interest and that is ordinarily occupied by the spouses as their family residence, or, if separated, was ordinarily occupied at the time of separation. More than one property can qualify (for example, a house and a cottage).

What “ordinarily occupied” means in real life

Courts look at reality, not labels. If a property functioned as a family residence (even seasonally, like a cottage), it can be caught by the definition. The key is the family’s pattern of use at the relevant time.

Important boundary: married vs. common-law

Ontario’s “matrimonial home” protections in the Family Law Act are built around the definition of “spouse” as married (or a void or voidable marriage entered in good faith). That’s why common-law partners often do not get the same automatic “matrimonial home” consent protections, though they may have other legal claims (trust or unjust enrichment) depending on facts.

Nihang Law Insight

In transactions, confusion often comes from people using “spouse” socially (common-law) versus legally (married). Clearing that up early can save weeks of delay when financing and closing are already in motion.

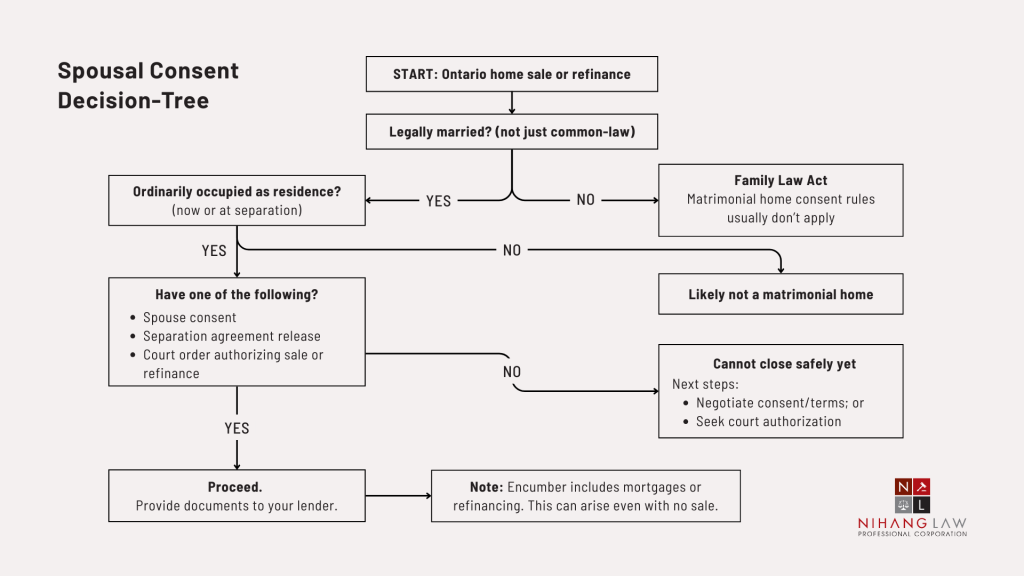

When Does Ontario Law Require Spousal Consent to Sell or Refinance?

If the property is a matrimonial home, no spouse may dispose of or encumber an interest in it unless the other spouse joins in or consents, the spouse has released rights by a separation agreement, or a court order authorizes the transaction (or releases the property from the Part).

This matters because “encumber” includes mortgaging/refinancing—so the issue can arise even when there is no sale.

Comparison table: common scenarios and what usually happens

Figure 1: Spousal Consent Decision-Tree

What Happens If Someone Tries to Sell Without the Non-Owner Spouse’s Consent?

A sale or mortgage done contrary to the spousal consent rules may be set aside by the court, unless the buyer/lender acquired the interest for value, in good faith, and without notice that the property was a matrimonial home at the relevant time. Ontario law also recognizes sworn statements as deemed proof in many conveyancing situations.

The two practical “pressure points” in real deals

- Deal certainty: Even if a buyer might ultimately argue “good faith without notice,” most buyers and lenders don’t want litigation risk attached to the home.

- Closing mechanics: Ontario conveyancing commonly relies on statutory statements about marital status and occupancy; if anything feels inconsistent, lawyers often pause to protect clients and insurers.

Nihang Law Insight

From a risk standpoint, spousal consent isn’t just a “family law issue”—it becomes a title and lender issue. Once flagged, it rarely disappears without a clear paper trail (consent, separation agreement, or court order).

What if the Spouse Refuses to Sign (or Can’t Be Found?)

Ontario courts can step in. On application, the court may determine whether a property is a matrimonial home and can authorize a sale or mortgage where the spouse cannot be found, is not capable of consenting, or is unreasonably withholding consent—often with conditions (such as alternate housing arrangements or financial safeguards).

Practical options (from least to most adversarial)

- Negotiated consent with terms: Sometimes the non-owner spouse will consent if there’s a clear written plan for interim housing, holdback, or how sale proceeds will be preserved pending equalization/support discussions.

- Separation agreement route: If the spouses sign an agreement releasing Part II rights, that can satisfy the statutory pathway in many cases.

- Court authorization: If negotiation fails, the statute expressly contemplates court authorization and conditions.

- Partition Act litigation (when jointly owned): Where the home is jointly owned, one party may seek a sale order under the Partition Act, but the family-law context can complicate timing and relief.

What Should Sellers, Buyers, and Spouses Do During a Live Transaction?

Treat spousal consent as an early due-diligence item, not a closing-day formality. Sellers should disclose marital/occupancy realities to their lawyer early; buyers should request confirmations and conditions if risk is apparent; and non-owner spouses should get advice before signing anything. Early clarity reduces failed closings and emergency motions.

Seller-side checklist (risk control)

- Tell your lawyer immediately if you are married, even if separated.

- Explain whether the home was ordinarily occupied as a family residence at separation.

- If consent may be difficult, discuss strategy before accepting a tight closing date.

- If refinancing, expect the lender to ask similar questions (encumbrance is covered). Buyer-side checklist (deal certainty)

- Ask whether the seller is married and whether the property is/was a matrimonial home.

- Consider clauses requiring delivery of spousal consent or a court order by a set date.

- Be wary of “we’ll sort it out later” assurances—this often becomes a last-minute collapse.

Non-owner spouse checklist (protecting rights responsibly)

- Confirm your status as a married spouse under the Act.

- Understand what you’re signing: “consent” can change leverage quickly.

- If safety is an issue, prioritize legal advice and safety planning (including court protections where appropriate).

What is the Step-By-Step Roadmap to Resolve a Spousal Consent Problem?

Most spousal-consent disputes follow a predictable roadmap: confirm whether the home legally qualifies, gather proof of marriage and occupancy history, attempt negotiated consent or a separation agreement release, and—if necessary—bring a court application for authorization to sell or mortgage. The earlier you start, the fewer closing deadlines you miss.

1. Confirm legal status

- Are you legally married (or in a void/voidable marriage entered in good faith)?

- Was the property ordinarily occupied as a family residence at separation (or currently)?

2. Collect the “proof package”

- Marriage certificate / evidence of marriage status

- Address history, emails, bills, school records, insurance showing ordinary occupation

- Any separation agreement drafts or prior court orders

3. Pick a resolution path

- Consent: negotiate and document the terms

- Separation agreement release: where appropriate under the statute

- Court authorization: for missing/incapable/unreasonably refusing spouse

4. Protect the transaction

- Update the closing timetable and conditions

- If you’re the buyer, ensure your lawyer has clear confirmations before waiving conditions

What are the Most Common Mistakes that Create Closing-Day Chaos?

Most spousal-consent crises come from delay and incomplete disclosure. People assume “not on title means no rights,” accept aggressive closing dates, or provide inconsistent statements about marriage and occupancy. These mistakes often force urgent renegotiation, extra legal cost, or court filings that could have been avoided with early planning.

- Assuming title ownership controls everything (it doesn’t for matrimonial homes).

- Treating “separated” as “divorced” for consent purposes.

- Waiting until after firm offers to raise spousal consent with your lawyer.

- Listing or accepting offers with unrealistic closing dates when consent is uncertain.

- Using informal messages instead of a properly drafted separation agreement release.

- Buyers waiving conditions without confirming spousal-consent risk.

- Not considering special regimes (for example, homes on reserve lands).

Frequently Asked Questions About Spousal Consent and the Matrimonial Home

These FAQs cover the questions Ontario buyers, sellers, and spouses most often ask when a non-owner spouse’s signature becomes a condition of closing. The common thread is that “matrimonial home” status triggers special protections and court remedies under Ontario law, and timing is usually the biggest practical risk.

Can my spouse stop me from selling my house if they’re not on title?

If you are married and the property is a matrimonial home, Ontario law generally prevents you from selling or mortgaging it without your spouse’s written consent, a separation agreement release, or a court order. This can apply even when only one spouse is the registered owner.

Does this apply if we are separated but not divorced?

Often yes. The definition focuses on whether the home was ordinarily occupied at the time of separation. Separation alone does not automatically remove the requirement. A proper separation agreement release or a court order may be needed to proceed safely.

Can the court force a sale if my spouse refuses to sign?

The court can authorize a sale or mortgage where the spouse cannot be found, cannot consent, or is unreasonably withholding consent, and the court may impose conditions (for example, alternative accommodation or financial safeguards). This is fact-driven and requires evidence.

What if I sold already? Can the deal be undone?

Potentially. Ontario law allows a transaction that violates the consent rule to be set aside, unless the buyer/lender acquired the interest for value, in good faith, and without notice that the property was a matrimonial home. That exception can be litigated and is risk-heavy.

Are common-law partners covered by the same “matrimonial home” consent rule?

Typically no, because the Family Law Act’s matrimonial home protections are structured around “spouse” as a married relationship (or void/voidable marriage in good faith). Common-law partners may still have other remedies (like trust/unjust enrichment claims), but the consent rule is different.

Does refinancing require spousal consent too?

It can. The statute covers not only disposing (selling) but also encumbering an interest in a matrimonial home—meaning mortgages and many refinances can trigger the same consent or court-order requirement.

Can a buyer protect themselves from spousal-consent risk?

Buyers can reduce risk by asking early questions about marital status and occupancy, using conditions/undertakings where needed, and ensuring the seller’s lawyer provides the appropriate confirmations commonly used in Ontario conveyancing. If the story is unclear, caution is warranted.

Does the rule change if the home is on a First Nation reserve?

Often yes. Homes on reserve lands may fall under a federal regime (Family Homes on Reserves and Matrimonial Interests or Rights Act), which has its own consent and court-authorization framework. You need reserve-specific legal analysis.

What’s the Takeaway for Ontario Buyers and Sellers?

In Ontario, a married non-owner spouse can legitimately block the sale or refinancing of a matrimonial home unless the spouse consents, rights are properly released in a separation agreement, or a court authorizes the transaction. The practical lesson is simple: raise this early—because waiting until closing is when it becomes expensive.

If you’re in the middle of a sale, refinance, or separation and spousal consent is becoming an obstacle, getting advice early can help you choose the cleanest path—negotiated consent, agreement-based release, or court authorization—without gambling on a last-minute rescue.

Reminder: Nothing here guarantees an outcome; timelines and remedies depend on evidence, urgency, and the court’s discretion.

If you need help assessing whether your property is a matrimonial home, what documents you need, or how to move a transaction forward lawfully, contact Nihang Law today. We aim to give clear and practical advice that protects both your legal position and your closing timeline.

Sources & References

- Family Law Act, R.S.O. 1990, c. F.3 (Ontario)

https://www.canlii.org/en/on/laws/stat/rso-1990-c-f3/latest/ - Partition Act, R.S.O. 1990, c. P.4 (Ontario)

https://www.canlii.org/en/on/laws/stat/rso-1990-c-p4/latest/rso-1990-c-p4.html - Non-Family Law Statutes That Family Lawyers Need to Know: The Partition Act (Ontario Bar Association)

https://www.oba.org/non-family-law-statutes-that-family-lawyers-need-to-know-the-partition-act/ - Family Homes on Reserves and Matrimonial Interests or Rights Act, S.C. 2013, c. 20 (Federal)

https://laws-lois.justice.gc.ca/eng/acts/F-1.2/page-2.html - O. Reg. 367/90: General (Family Law Act) (Ontario Regulation)

https://www.canlii.org/en/on/laws/regu/rro-1990-reg-367/latest/rro-1990-reg-367.html

Thank you for reading this post, don't forget to subscribe!