23rd February 2026BY Nihang Law

Wage Garnishment in Ontario: Rules, Wage Limits, Bank Account Seizures & Step-by-Step Options

Whether you are a homeowner, an employee, or a small business owner, few things feel more urgent than money suddenly moving without your say-so. In a wage garnishment situation in Ontario, your paycheque can shrink before you have even had a chance to breathe. If the garnishment targets a bank account, it can feel even harsher: payments bounce, pre-authorized bills fail, and you are left trying to understand what happened.

On the other side of the table, creditors often feel stuck too. You did the work, delivered the product, or won your case in court — and the debtor still will not pay. Garnishment can be one of the tools that may turn a paper judgment into real money.

This guide explains what garnishment is in Ontario, how wage garnishment and bank garnishment typically work, what limits apply, and what practical steps you can take next.

Quick Start: Pick Your Situation

Pick the situation that fits you right now:

- My wages are being garnished: Start with “How much can be taken?” and then “Step-by-step process for debtors.”

- My bank account was frozen, or money was taken: Read “Wage vs. bank account garnishment” and “Common mistakes.”

- I am owed money, and the debtor will not pay: Go to “Step-by-step process for creditors.”

- I am an employer or payroll person served with papers: Go to “Step-by-step process for employers and banks.”

- This is child or spousal support: Go to “Support enforcement and FRO: different rules.”

- This is CRA (tax debt): Go to “CRA Requirement to Pay (RTP): a different system.”

What is Garnishment?

Garnishment is a legal procedure that may redirect money that would otherwise go to a debtor – often wages or money in a bank account – and apply it to a debt instead. In many cases, garnishment is used after a court has made a money order or judgment, but some government or support enforcement processes can operate under different rules.

Ontario’s Rules of Civil Procedure set out the civil garnishment process, including how a creditor can garnish a debt payable to the debtor by another person (often an employer or bank).

Key Terms in Plain English

- Creditor: the person or business owed money.

- Debtor: the person or business that owes the money.

- Garnishee: the third party who owes money to the debtor – commonly an employer (wages) or a financial institution (bank account).

Wage Garnishment vs. Bank Account Garnishment

Both (wage and bank account) are forms of garnishment under Ontario garnishment rules, but they often feel very different in real life.

Wage garnishment in Ontario usually affects pay over time, because the garnishee is your employer and the amounts are taken from each pay period (subject to wage‑protection limits). Those wage limits come from Ontario’s Wages Act.

Bank account garnishment, meanwhile, typically targets money that is payable by a financial institution to the debtor. Because the Wages Act protections apply to “wages,” bank garnishment does not work like a simple “20% of your balance” rule. Service rules and timing can be technical, especially for financial institutions, so the paperwork matters. The civil garnishment mechanics are set out in Rule 60.08 of the Rules of Civil Procedure.

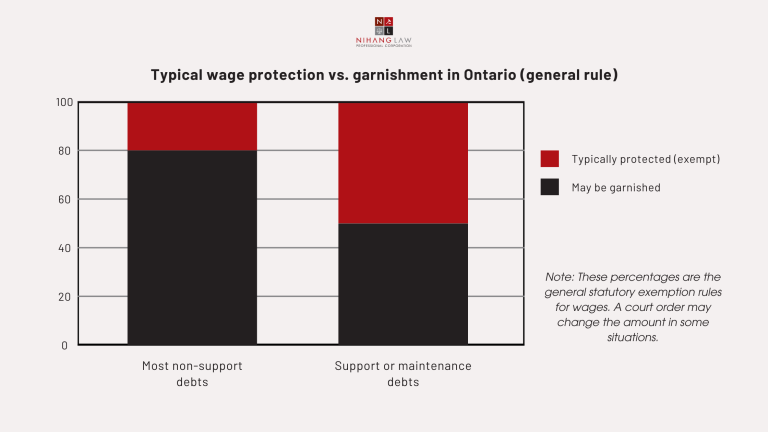

How Much Can Be Taken from Wages in Ontario?

This is usually the first question people ask about wage garnishment. Ontario law protects a portion of wages from seizure or garnishment.

For many non‑support debts, the Wages Act says 80% of a person’s wages are exempt from seizure or garnishment (meaning up to 20% may be taken), unless a court orders otherwise.

For support or maintenance enforcement, the Wages Act provides a different threshold: 50% of wages are exempt (meaning up to 50% may be taken), again subject to what a court orders.

Court forms also warn that the protected or garnishable portion may be increased or decreased only by court order (see the Small Claims Court Notice of Garnishment – Form 20E and the family law Notice of Garnishment – Form 29B).

Chart 1. Typical wage protection vs. garnishment in Ontario (general rule)

When Garnishment is Available (and when it isn’t)

In many everyday civil situations, garnishment is a post‑judgment tool. In other words, the creditor has already obtained a court order or judgment for money, and is now trying to collect. Small Claims Court materials reflect this: the creditor has obtained a court order against the debtor before issuing a notice of garnishment (see Form 20E).

However, not every garnishment comes from a typical lawsuit:

Family support enforcement: Support collection may run through Ontario’s Family Responsibility Office (FRO) and related legislation (see the Family Responsibility and Support Arrears Enforcement Act, 1996 and the Ontario Court of Justice overview on support enforcement).

CRA collection: The CRA can issue a Requirement to Pay (RTP) (and related notices) that may direct third parties to pay amounts to the Receiver General. CRA guidance explains that a court order is generally not required for RTP garnishments, and the underlying authority appears in provisions such as section 224 of the Income Tax Act.

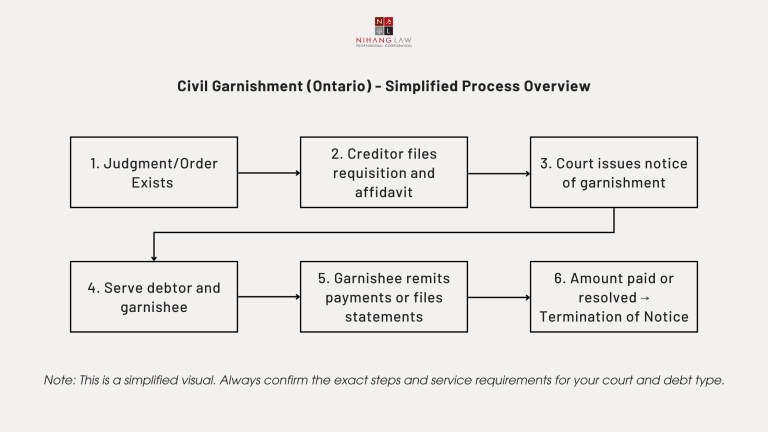

Ontario Civil Garnishment Step-by-step Process

If You Are the Creditor (you are owed money)

This is the typical sequence when you are trying to collect a civil debt by garnishing wages or a bank account. Your steps may vary depending on whether the order is from Small Claims Court or the Superior Court of Justice, but the core ideas are similar.

- Confirm you have an enforceable money judgment or order (and confirm the correct court file details).

- Identify the garnishee (for wage garnishment, the employer; for bank garnishment, the relevant financial institution).

- Prepare the court materials. Under the Rules of Civil Procedure, civil garnishment involves filing a requisition and an affidavit setting out key details (amounts paid, amounts owing, debtor information, and the garnishee information).

- Have the notice of garnishment issued by the court, then serve the debtor and the garnishee in the required way (the Rules outline what must be served).

- Monitor compliance. For example, civil forms such as the Superior Court Notice of Garnishment (Form 60H) warn the garnishee to pay within 10 days, and permit a $10 deduction per payment for the garnishee’s costs.

- If the debt is paid, terminate properly. The Rules contemplate a notice of termination when the judgment amount has been satisfied.

Where to verify the exact procedural requirements: Rule 60.08 (Garnishment) in the Rules of Civil Procedure, the Small Claims Form 20E, and the Superior Court Form 60H.

Chart 2. Civil Garnishment (Ontario) – Simplified Process Overview

If you are the debtor (your wages or account is being garnished)

If you have just discovered a garnishment, the goal is to move from panic to control. Here is a practical sequence that often helps.

- Confirm what you were served with and who issued it (Small Claims, Superior Court, FRO, or CRA). The best next step depends on the source.

- Figure out what is being targeted (wages, bank account, or both) and confirm the employer/bank details on the paperwork.

- Get clarity on the numbers: what amount is claimed, what interest or costs are included, and what has already been paid, if anything.

- If there is a real dispute or you need a change, act quickly. The Rules of Civil Procedure provide for a garnishment hearing process where the court can determine issues related to the notice.

- Consider a negotiated payment plan or settlement if it will stop ongoing disruption and costs (especially where a debtor can make steady payments).

- If the garnishment relates to support arrears or CRA debt, treat it as its own category – the tools, timelines, and options may be different.

Helpful starting points for forms and process: Small Claims Form 20E, Rule 60.08, and CRA’s overview on garnishing income and accounts.

If you are an employer or bank (the garnishee)

Being served with garnishment papers can create real administrative risk. The safest approach is to identify the issuing authority, calendar the deadlines, and follow the form’s instructions closely.

- Confirm the notice type and issuing authority (court vs FRO vs CRA).

- Calendar deadlines immediately. Civil garnishment forms, such as Form 60H, refer to 10 days to pay (or provide a statement if you cannot pay).

- Deduct only what the notice requires and only from the correct source (wages vs other payments).

- Pay the correct recipient (for example, Small Claims forms warn that paying anyone other than the clerk may leave you liable to pay again).

- Keep a clean internal record of payments and correspondence in case of later disputes.

Key documents to review: Form 60H and Form 20E (plus CRA RTP guidance if CRA is involved).

Support Enforcement and FRO: Different Rules

If the debt is child support or spousal support, Ontario uses a different enforcement framework. Two practical differences show up quickly: (1) the percentage that may be deducted from ongoing income is usually higher than a typical civil wage garnishment, and (2) certain lump-sum payments can be treated differently.

Ontario’s Family Responsibility and Support Arrears Enforcement Act, 1996 sets a general cap that the total amount deducted by an income source and paid under a support deduction order shall not exceed 50% of the net amount owed by the income source to the payor (subject to the statute and any court order).

The Act explains “net amount” by listing common deductions such as income tax, CPP, EI, union dues, and other prescribed deductions. It also provides that up to 100% of an attachable income tax refund or other attachable lump-sum payment may be deducted and paid under a support deduction order.

Family court garnishment materials summarize these ideas in practical terms (see Form 29B).

CRA Requirement to Pay (RTP): A Different System

Many people assume every garnishment requires a court judgment. CRA collections are often different.

CRA guidance explains that the CRA can issue a Requirement to Pay (RTP) (and related notices) to require a third party – such as an employer, bank, or someone who owes money to the taxpayer – to pay amounts to the Receiver General. CRA materials also state that a court order is generally not required for RTP garnishments.

The legal authority is grounded in federal law, including provisions such as section 224 of the Income Tax Act. If CRA is involved, it is usually worth getting quick advice because the timelines, priorities, and negotiation options may differ from a typical civil judgment enforcement process.

Common Mistakes and How to Avoid Them

If you are the debtor

- Ignoring the first notice and hoping it goes away. Garnishment often continues until it is terminated, varied by a court, or the debt is paid.

- Mixing up debt types (civil judgment vs support vs CRA). The caps and tools can be different.

- Waiting too long to ask for help when you have a real dispute or hardship. Civil rules include a garnishment hearing mechanism in the right case.

If you are the creditor

- Starting enforcement without the correct paperwork or service. Garnishment is document-driven, and errors can cause delay and cost.

- Serving the wrong entity or leaving out key garnishee details (for employers: correct legal name; for banks: correct branch or service details).

- Forgetting to terminate the garnishment after the amount is paid, which can create avoidable disputes.

If you are an employer or bank (garnishee)

- Missing the deadline to pay or provide the required statement. Civil forms such as Form 60H highlight strict timelines.

- Paying the wrong recipient. Small Claims materials warn that paying anyone other than the clerk may leave you liable to pay again.

- Over-deducting from wages without checking wage-protection limits and the exact terms of the notice.

Where to double-check the official wording: Form 60H, Form 20E, and the Wages Act.

Frequently Asked Questions

How do I know whether this is wage garnishment or something else?

Check who issued it and what form it is. Court documents often look different from CRA or support enforcement notices. If it is court-issued, compare it to official forms like Small Claims Form 20E or civil Form 60H.

How much of my pay can be garnished in Ontario?

For many non-support debts, the Wages Act exempts 80% of wages (so up to 20% may be garnished), and for support it exempts 50% (so up to 50% may be garnished), unless a court orders otherwise.

Does garnishing wages in Ontario always require a court judgment?

Often, civil wage garnishment is tied to a judgment or order (Small Claims materials assume a court order exists). But support enforcement and CRA tools can operate under different legal authority.

Is bank account garnishment limited to 20% like wages?

Not typically. Wage protections come from the Wages Act and apply to wages. Bank garnishment is governed by the civil rules about debts payable to the debtor, so the practical impact can be different.

How long can a court-issued notice of garnishment last?

Ontario’s Rules of Civil Procedure set a default period that a notice of garnishment remains in force (and also address renewal). Check Rule 60.08 for the current wording.

Can I challenge or change a garnishment amount?

Sometimes. The civil rules provide for a garnishment hearing process where the court can determine issues related to the notice. Support and CRA situations may have different processes.

If I am an employer, do I have to comply?

If the notice is valid and properly served, employers and banks generally must comply as garnishees. If you cannot comply (for example, you do not owe money to the debtor), the civil rules provide a statement process.

I am a small business creditor – Is garnishment my only option?

No. Garnishment is one tool. Depending on the debtor’s assets and where they keep money, other enforcement steps may be more effective. A short legal review can help you choose the best path.

In Summary

Wage garnishment is one of the main ways a creditor may collect money after a judgment – and it is also one of the most disruptive tools a debtor can face.

In Ontario, wage garnishment rules are shaped by two big ideas:

1. Wages have statutory protection (often 80% exempt for many non-support debts, and 50% exempt for support), and

2. The exact process is paperwork-driven under the Rules of Civil Procedure, with different streams for support enforcement and CRA.

If you are dealing with wage garnishment issues in Ontario, the most important first step is identifying what type of garnishment it is (civil, support, or CRA) and then acting quickly on the next practical step – whether that is enforcing, negotiating, or bringing the issue before the court.

How Nihang Law Can Help

If you are trying to collect a debt, we can help you assess whether garnishing wages or a bank account is the right enforcement tool, prepare the paperwork, and avoid costly service mistakes.

If you are being garnished, we can review what was served, confirm whether the correct process was followed, and help you consider practical options – including negotiation, a court process where appropriate, or a plan to stabilize cashflow.

To speak with a legal professional who is adept in civil litigation, contact Nihang Law Professional Corporation to book a consultation.

Disclaimer: This article is general information, not legal advice. Wage garnishment rules in Ontario and outcomes depend on your facts. If you need advice, speak with a qualified legal professional.

Thank you for reading this post, don't forget to subscribe!