27th March 2026BY Qasim Nihang

Title Fraud in Ontario: What Title Insurance Actually Pays in a Fraud Scenario

Title insurance is not a promise of automatic reimbursement the moment fraud is discovered. Instead, in a covered fraud scenario, it operates primarily as a defence-and-resolution product.

If you are navigating title fraud in Ontario, here is what you need to know:

Title insurance fixes the problem first: Rather than simply cutting a cheque, the insurer will often step in to pay legal fees, defend your title in court, or actively remove the fraudulent registration.

Owner vs. Lender Coverage: An owner’s policy protects the homeowner’s title, while a lender’s policy strictly protects the bank if the mortgage is invalid. You cannot rely on a lender’s policy to protect you personally.

The Statutory Alternative: Ontario’s Land Titles Assurance Fund (LTAF) provides a separate, provincial avenue for compensation under the Land Titles Act, completely distinct from private insurance.

Last updated: March 2026

Imagine this scenario: You own your home, and your mortgage may even be paid off. Then suddenly, a letter arrives about a mortgage you never signed or a transfer you never authorized.

At that point, most people are not asking abstract questions about insurance law. They want to know who fixes the title, who pays the lawyer, and whether this fake mortgage will cost them a sale, a refinance, or their savings.

That is exactly where title insurance matters. But the scope of coverage is narrower than many people expect. While title insurance can respond strongly in fraud cases, it is still strictly governed by policy wording, insured status, exclusions, and claims-handling rules. In Ontario, understanding this reality early on can prevent false assumptions and expensive delays.

Quick Start: Pick Your Path

Buying or refinancing now:

- Confirm whether you are getting only a lender’s policy or also an owner’s policy.

Already own the property:

- Check whether you ever received an owner’s policy at purchase or refinance, and locate the policy number.

Suspected fraud discovered:

- Pull title information fast, notify your lawyer and insurer, and preserve every notice and document.

Claim resistance or denial:

- Review the exact policy wording, endorsements, notice requirements, and complaint path before assuming the insurer is right.

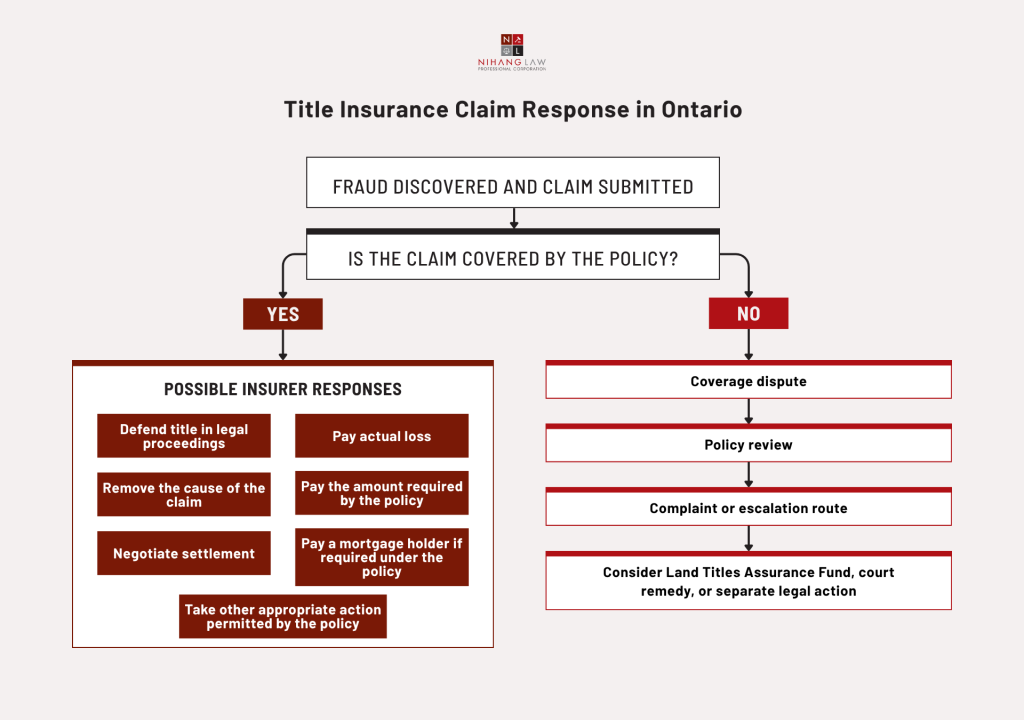

What Does Title Insurance Actually Do After Title Fraud Is Discovered?

In a covered fraud case, title insurance is rarely just a cash-payment product. Instead, it operates primarily as a problem-solving tool designed to actively fix the underlying issue.

The Insurer’s Menu of Options

A look at standard Canadian owner policies (such as a sample from TitlePLUS) shows exactly why consumers often misunderstand the product. Once a claim is reported, the insurer is not just obligated to pay the actual loss; they have a menu of options to resolve it. They may step in to:

Defend your title in court and cover the associated legal costs.

Actively litigate to remove the fraudulent registration.

Negotiate a formal settlement with the involved parties.

Compensate the actual loss or pay off a protected lender.

The Limits of Coverage

The Financial Services Regulatory Authority of Ontario (FSRA) confirms that while this one-time-premium product offers robust protection against title-related losses and legal expenses, it does not act as a blanket guarantee.

Crucially, FSRA stresses that title insurance does not replace independent legal advice, and the exact scope of your coverage will always depend on the strict wording of the policy itself.

Title insurance is often a problem-solving product first and a cash-payment product second.

The visual below shows how a fraud claim may branch once it is reported to the title insurer.

Nihang Law Insight

In real title fraud files, the urgent issue is often not only “How much money will I get?” It is “How do I clear title fast enough to stop enforcement notices, save a sale, or protect my refinancing?” Policy wording that gives the insurer control over defence strategy can matter just as much as the dollar limit.

What Kinds of Title Fraud Are Usually Covered by Title Insurance?

While every policy is different, residential title insurance commonly covers the major forms of title fraud, including forged property transfers, fraudulent ownership changes, forged mortgage discharges, and fraudulent new mortgage registrations.

The Mechanics of the Crime

According to the Financial Services Regulatory Authority of Ontario (FSRA) and major insurers like FCT and Stewart, these covered crimes typically involve criminals using stolen personal information, impersonation, or forged powers of attorney to secretly alter a home’s title or secure a fake mortgage.

Ongoing, “Post-Closing” Protection

This brings up a crucial but often overlooked benefit for Ontario owners: many residential policies are designed to respond not only to title defects that existed before closing, but also to these types of post-closing fraud. That ongoing, future-facing protection is exactly why title insurance is so vital in mortgage fraud scenarios involving longtime owners with paid-off homes.

The Fine Print Warning

Despite these broad protections, you still must read your policy, as not every fraud-related loss is automatically insured. The exact scope of your coverage will always depend heavily on your specific policy version, property type, endorsements, and exclusions.

Who Actually Gets Paid in a Fraud Case: The Owner, The Lender, or Someone Else?

It depends on who is insured and what specific loss occurred. FSRA clearly distinguishes between the two main policy types: an owner’s policy and a lender’s policy.

An owner’s policy protects the homeowner’s title-related losses up to the policy’s maximum amount, while a lender’s policy protects the lender if the mortgage is invalid, usually up to the mortgage amount.

Additionally, Ontario’s Land Titles Assurance Fund (LTAF) provides a separate, statutory compensation route for specific fraud or registry errors.

Quick Comparison Guide

To understand exactly who is protected and how, here is how the three avenues compare:

Comparison Point | Owner’s Title Insurance | Lender’s Title Insurance | Land Titles Assurance Fund |

Who is protected? | The property owner. | The mortgage lender. | A person who qualifies for compensation under Ontario’s statutory scheme. |

What is the main purpose? | To protect the owner’s interest in the property against covered title-related loss. | To protect the lender’s mortgage security if the insured mortgage is affected by title defects or fraud. | To provide a separate statutory compensation route for certain fraud-, omission-, or registration-error losses. |

What kinds of problems may it respond to? | Certain fraud-related title issues, ownership defects, or other covered title problems affecting use, ownership, or marketability. | Invalid or unenforceable mortgages, title defects affecting priority, and other insured risks under the lender policy. | Certain financial losses caused by fraud, omissions, or errors in Ontario’s land registration system. |

What may be paid or covered? | Depending on the policy, legal fees to defend title, costs to resolve the title issue, and compensation for actual covered loss up to the policy limit. | Depending on the policy, the lender’s financial loss, legal costs, and other amounts covered under the lender policy. | Compensation for qualifying financial loss and, in some cases, reasonable legal or related costs, subject to statutory requirements. |

Who decides the claim? | The title insurer, based on the policy wording, endorsements, exclusions, and facts of the claim. | The title insurer, based on the lender policy and facts of the loss. | Ontario’s statutory claims process under the Land Titles Act. |

What is the main limitation? | Coverage depends on policy wording, exclusions, endorsements, notice requirements, and policy amount. | It protects the lender, not the homeowner personally. | It is not private insurance, and eligibility is limited by legislation and claim requirements. |

What is the most common misunderstanding? | That any fraud automatically results in a direct cash payout to the owner. | That the lender’s policy also protects the homeowner. | That it works the same way as title insurance. |

When is it most relevant in a fraud case? | When the owner needs title defence, fraud-related loss protection, or help resolving a covered title issue. | When fraud affects the lender’s mortgage security or enforceability. | When there is a qualifying fraud- or registry-related loss and statutory compensation may be available. |

Concurrent Payment Paths

The practical takeaway is that a fraudulent mortgage may produce different payment paths at the same time. While you (the owner) is more focused on title restoration and legal defence, the lender will seek payment under their own policy because their security (the fake mortgage) is worthless.

A crucial warning for homeowners: you should never assume a lender’s policy protects you personally.

The Statutory Safety Net

Furthermore, while insurance handles the immediate policy claims, the Land Titles Assurance Fund exists under the Land Titles Act as a broader safety net. Depending on the facts of the case, the LTAF may compensate for other financial losses and reasonable legal costs related to the fraud that fall outside of your private coverage.

The Risk of Escalation

Because the insurance claims, the title restoration, and the potential for competing property interests must be managed together, it is vital to speak with an Ontario real estate lawyer early. If the dispute involves the validity or priority of a mortgage, the problem can quickly escalate from an insurance claim into formal and expensive mortgage litigation.

How Does A Title Insurance Claim Usually Unfold In Ontario?

A strong response to title fraud in Ontario requires urgency, strict documentation, and simultaneous action.

Because a claim involves an internal insurance investigation happening at the exact same time as a formal land-registry or court process, homeowners must act immediately to secure evidence, notify all relevant authorities, and involve a legal professional to navigate the overlapping systems.

The Standard Roadmap

Based on guidance from the Financial Services Regulatory Authority of Ontario (FSRA) and standard policy procedures, a typical claim unfolds through these core steps:

- Confirm your coverage: The first step is to locate your policy details and verify that the specific problem may be covered.

- Submit written notice immediately: FSRA advises submitting claims as soon as possible. You must do this in writing, with policy number, contact information, details of loss, and supporting documents.

- Secure the title evidence: Gather official title information—such as a parcel register and copies of registered instruments using Ontario’s OnLand registry. These specific documents are the foundation of any fraud allegation.

- Report and escalate where needed: Ontario’s fraud guidance says to act quickly, report to police, tell your lawyer or adviser, and contact the local land registry office or the Director of Titles.

- Cooperate with the insurer: Standard policy wording requires the insured to cooperate, provide documentation, and avoid prejudicing recovery rights. Warning: The insurer generally retains the right to choose the legal counsel and may only reimburse settlement costs, legal fees, and expenses that it has explicitly approved in advance.

- Expect a chosen remedy, not necessarily cash: As noted earlier, the policy allows the insurer to choose how to resolve the problem. They may choose to defend your title in court, cure the defect, negotiate a settlement, or pay out the loss, depending on what makes the most sense for the claim.

When Might The Insurer Defend The Title Instead of Just Sending Money?

The Insurer’s Discretion to Defend

Quite often. Standard policy wording grants the insurer the discretion to choose exactly how to resolve a covered risk. Instead of just sending money, the insurer has the right—and the duty—to step in, hire lawyers, and actively fix the underlying title issue before any final loss payment is calculated.

“Funded Litigation Management”

A look at the TitlePLUS sample policy illustrates this clearly. Because the insurer is managing and paying for the legal maneuvers, a homeowner often experiences title insurance as funded litigation management rather than an immediate financial reimbursement. To resolve the claim, the insurer can choose to:

Defend your title in court and pay the associated legal costs.

Negotiate a formal settlement with the involved parties.

Take active steps to remove the cause of the claim entirely.

The Importance of Technical Wording

The Ontario Court of Appeal’s decision in Nodel v. Stewart Title Guaranty Company serves as a stark reminder that these fraud claims often turn on highly technical wording. In that case, a lender had mortgage fraud coverage, but the dispute centered on a policy exception simply because funds were paid to the borrower’s lawyer in trust rather than directly to the borrower.

While the Court ultimately upheld the coverage, the Nodel case proves that specific policy wording and transaction mechanics will materially affect how your fraud claim is handled.

Legal Perspective

One of the most expensive mistakes is treating a fraud claim as if the only issue is whether fraud happened. In reality, the fight may also be about who was insured, what precise loss is claimed, whether notice was prompt, whether costs were approved, and whether a policy exception is engaged.

What Falls Outside Coverage or Commonly Creates Disputes?

The Three Main Causes of Denials

Disputes and denied claims typically stem from three main issues: strict policy exclusions, broken conditions, or simple assumption errors. Even if a title problem is very real and financially severe, your claim can be denied entirely if it falls outside the explicitly insured risks or if you fail to follow the insurer’s strict procedural rules.

Strict Policy Exclusions

The Financial Services Regulatory Authority of Ontario (FSRA) outlines several common scenarios where a policy simply will not pay out. This reinforces the reality that while title insurance is broad, it is not unlimited. Common exclusions include:

Title defects you already knew about before buying the policy.

Environmental hazards and Indigenous land claims.

Zoning by-law violations caused by your own post-purchase changes to the property.

Issues that would only have been discovered through a new property survey or inspection.

Procedural Traps That Void Coverage

Beyond straight exclusions, the fine print of the contract dictates exactly how you must behave during a claim. Your coverage can be significantly reduced—or voided entirely—if you fall into these procedural traps:

Unapproved Spending: Hiring lawyers or paying settlement costs without the insurer’s prior written approval.

Lack of Cooperation: Failing to fully cooperate with the insurer’s internal investigation or requests for documentation.

Prejudicing Rights: Taking independent actions that harm the insurer’s legal ability to recover the lost funds from the fraudsters or third parties.

Caps on Financial Payouts

Finally, even if your claim is perfectly valid and approved, your payment has a ceiling. A standard owner policy typically caps the insurer’s financial liability at the lesser of your actual financial loss or the total maximum amount of the policy.

Nihang Law Insight

Consumers often read the brochure and stop there. The brochure explains the product. The policy governs the claim. In a fraud file, the schedule, endorsements, exceptions, approval requirements, and insured-name details matter immediately.

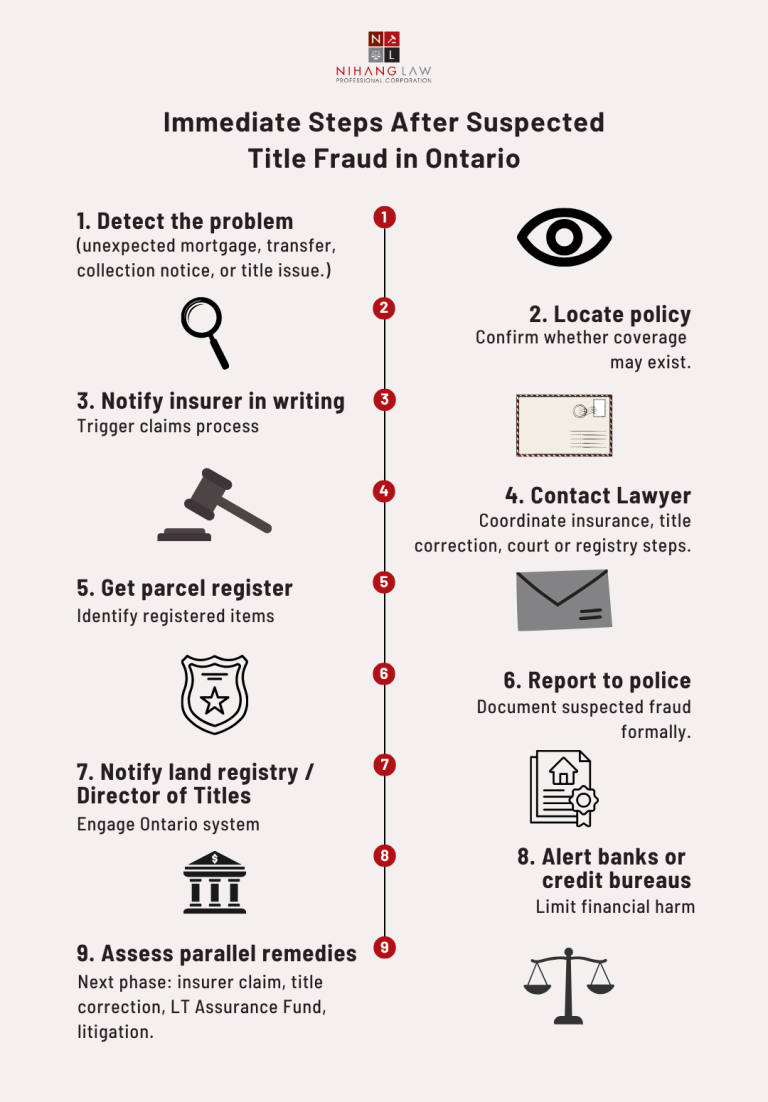

What Should You Do The Moment You Suspect Title Fraud?

A sense of urgency is essential because these files instantly become complex property and real estate disputes. Your primary objective is to protect your rightful ownership, remove the fraudulent registrations, and stop the financial damage from spreading before a pending sale or refinance collapses.

Your “First Day” Contact Checklist

The moment you suspect fraud, you must launch a coordinated response. Because you cannot rely on just one channel to fix the issue, your immediate strategy should involve:

Notifying your title insurer in writing.

Alerting your mortgage lender.

Reporting the crime to the local police.

Contacting the local land registry office or the Director of Titles.

Engaging an Ontario real estate lawyer.

Taking immediate credit-alert steps to mitigate any ongoing identity theft.

Securing the “Documentary Core”

To support this coordinated response, you must secure what Ontario’s official fraud guidance calls the “documentary core” of your claim. This involves pulling your official title records—specifically the parcel register and copies of the allegedly fraudulent instruments—directly through the provincial OnLand registration system.

Preserving the Physical Paper Trail

Finally, you must physically preserve every notice, letter, or envelope you receive. This strict paper trail will be required whether you are navigating an internal insurance claim, applying to the Land Titles Assurance Fund (LTAF), or seeking a court-ordered title rectification.

What Mistakes Make A Title Fraud Situation Worse?

The most common mistakes in a title fraud situation involve critical delays, wrong assumptions about coverage, and acting without the insurer’s approval. When a homeowner mishandles these initial steps, a straightforward insurance claim can quickly turn adversarial, escalating the matter from a standard closing issue into a much broader and more expensive civil litigation strategy.

To keep your claim on track and protect your coverage, avoid these critical missteps:

1. Procedural and Timing Mistakes

Waiting too long to give official written notice to the insurer.

Failing to pull the official parcel register and registered instruments quickly.

2. Dangerous Coverage Assumptions

Assuming a lender’s policy protects the homeowner personally.

Believing title insurance must automatically pay off a fraudulent mortgage on demand, rather than allowing the insurer to manage the resolution.

Treating the statutory Land Titles Assurance Fund (LTAF) as identical to a private insurance policy.

Forgetting that fine-print exclusions and endorsements may narrow what looked covered at first glance.

3. “Going Rogue” Without Approval

Spending money out of pocket without checking what the insurer must approve first.

Launching independent litigation or settling issues without understanding the insurer’s strict approval requirements.

Frequently Asked Questions

Does title insurance automatically pay off a fraudulent mortgage?

No. Automatic payout is not how these policies are typically structured. Instead of an immediate cash reimbursement, an insurer will usually exercise their right to actively defend your title in court, remove the fraudulent registration, or negotiate a resolution.

Can I buy title insurance after I already own the property?

Yes, in many cases. While it is typically purchased when you buy a property, the Financial Services Regulatory Authority of Ontario (FSRA) notes that “existing homeowner” policies are readily available. This is a crucial protective step for longtime owners who did not receive an owner’s policy at closing.

Does my lender’s title insurance protect me as the homeowner?

Usually no. FSRA explains that a lender’s policy protects the lender’s mortgage interest, while an owner’s policy protects the owner from covered title-related losses. A homeowner should never assume the bank’s coverage is the same as personal protection.

Will title insurance pay my legal fees in a fraud case?

It may. Standard policies generally cover the legal expenses involved in defending your title, and sample policy wording provides a duty to defend covered title litigation. However, the policy terms, strict insurer approvals, exclusions, and your insured status still dictate exactly what gets paid.

Can I still apply to the Land Titles Assurance Fund if I have title insurance?

Potentially, yes, but it is a separate regime. The Land Titles Assurance Fund (LTAF) compensates for certain financial losses due to fraud, omissions, and land-registration errors under Ontario law. Whether it applies—and how it interacts with your private insurance—depends entirely on the facts of your case and statutory criteria.

What if the fraud is discovered while I am trying to sell or refinance?

This is an urgent situation. Title must generally be cleared before a new transaction can close. Your immediate priorities are to pull the official parcel register, notify your insurer and your lawyer, and quickly determine whether the insurer will cure the title defect or compensate you before the pending deal collapses.

What if the insurer denies my coverage?

Start with the internal complaint process. FSRA advises that you should complain to the insurer first and obtain a “final position letter.” If the issue remains unresolved, escalating the dispute through the General Insurance OmbudService (GIO) or FSRA’s complaint route may become relevant.

Is title insurance mandatory in Ontario?

No. FSRA confirms that title insurance is not legally required in Ontario. That said, whether it is wise to obtain an owner’s policy is a different question entirely, especially since fraud, unknown liens, title defects, or survey-related risks can become incredibly expensive to resolve out of pocket.

Key Takeaways

Not A Blank Cheque

Title insurance in an Ontario fraud case is not a blank cheque—it is a highly structured defence mechanism. As we have explored, a covered claim does not guarantee an automatic payout to the homeowner. Instead, the insurer may choose to fund legal work, actively rectify the title, or strictly protect the lender.

A Coordinated Strategy is Essential

Because private insurance and the statutory Land Titles Assurance Fund (LTAF) operate under entirely different rules, you cannot rely on a single channel for relief. Your safest approach is a coordinated strategy that tackles the internal insurance claim, the underlying title defect, and the broader litigation risk simultaneously from day one.

Securing Prompt Legal Representation

When you are dealing with a suspicious transfer, a forged mortgage, or a denied insurance claim, your most critical next step is securing prompt legal representation to stop the financial damage from spreading.

Disclaimer: This article is intended for general information purposes only. The actual result in any title fraud matter depends heavily on your specific policy wording, endorsements, registration history, the facts of the identity theft, the lender’s position, and the exact steps taken immediately after discovery. Always seek prompt legal advice from an Ontario real estate lawyer regarding your specific situation.

How Nihang Law Help

Nihang Law can step in immediately to manage the complex, overlapping systems of a title fraud crisis. We assist Ontario homeowners by:

Thoroughly reviewing your official title records and complex policy wording.

Coordinating directly with the title insurer on your behalf.

Assessing your alternative statutory LTAF recovery options.

Executing urgent court interventions to correct the title and protect your rightful ownership.

Sources & References

FSRA – Understanding Title Insurance

Ontario – Compensation for Victims of Real Estate Fraud / Land Titles Assurance Fund background PDF

Ontario – Victims of Real Estate Fraud

Ontario – Order of the Director of Titles: Evidence of Fraud

OnLand – Parcel Register Options

FSRA – How to resolve a Property and Other Insurance complaint

TitlePLUS – Sample Existing Owner Policy and Endorsement

FCT – Understanding Title Insurance

FCT – Title Fraud: What Every Canadian Homeowner Needs to Know

Stewart Title – Coverage for Real Estate Title Fraud

Minicounsel summary of Karl Nodel v. Stewart Title Guaranty Company, 2018 ONCA 341

Thank you for reading this post, don't forget to subscribe!