11th March 2026BY Nihang Law

Ontario Estate Information Return: The 180-Day Deadline Every Estate Trustee Needs to Know

Last Updated: March 2026

In Ontario, an estate representative who receives an estate certificate (also known as probate) generally must ensure the Estate Information Return is received by the Ministry of Finance within 180 calendar days after the certificate is issued. That filing duty can still apply even where the estate is $50,000 or less and no Estate Administration Tax is payable. If information later turns out to be wrong or incomplete, an amended return may also be required, often within 60 days of discovery and generally within four years of issuance of the certificate. Missing the deadline can expose the estate to audit, reassessment, and offence provisions.

When a loved one dies, families are often focused on funeral arrangements, locating documents (or dealing with the consequences of not having a will), access to bank accounts, selling or securing property, and simply getting through the first few months. The Estate Information Return can feel like one more form in a long list of paperwork. The problem is that Ontario treats it seriously.

The 180-day deadline is not just an administrative suggestion. It is part of a broader statutory system that allows the Ministry of Finance to review valuations, issue assessments, and in some cases pursue offences for non-compliance or false or misleading reporting. For many estate trustees, the real risk is not bad faith. It is underestimating how long it takes to identify assets, confirm date-of-death values, and decide whether a correction or amended return is required.

Legal disclaimer: This article is general legal information for Ontario readers only. It is not legal advice. Estate planning outcomes depend on the certificate issued, the asset mix, valuation evidence, and whether the Ministry of Finance later reviews the file.

Quick Start: Pick Your Path

I just received probate or a small estate certificate.

- Count 180 calendar days from the issue date and build the return package early.

I used estimated values in the probate application.

-

You may need an initial return and then an amended return once actual values are confirmed.

I discovered a new asset after probate.

-

A court filing and then an amended return may both be required.

I think the original return was wrong.

-

The 60-day amendment clock may already be running.

I already missed the deadline.

-

Do not assume the problem will disappear; late filings can still be assessed or reassessed at any time.

When Does the 180-Day Clock Start, and Who Has to File?

In Ontario, the initial Estate Information Return generally must be received by the Ministry of Finance within 180 calendar days after the estate certificate is issued. The obligation applies to anyone who receives a certificate of appointment of estate trustee—whether named in a document or appointed by the court because the deceased died without a will—including cases where the estate owes no Estate Administration Tax because the estate value is $50,000 or less.

The key trigger is the issuance of the estate certificate, not the date of death and not the date the probate application was submitted. Ontario’s guidance also makes clear that the return is required even where the estate is at or below $50,000 and no tax is payable, provided the person has received the relevant estate certificate. That point catches many first-time estate trustees by surprise.

There are some exceptions. The Ministry guide says a new return is generally not required in certain situations, including some succeeding estate trustee certificates, certificates issued during litigation, applications made before January 1, 2015, and applications that were withdrawn or never resulted in a certificate. Those exceptions should be checked carefully against the exact certificate issued.

Ontario also now permits online filing through the Ministry of Finance’s online services page. The official forms repository states that beginning March 3, 2025, the Estate Information Return can be filed online, and the fillable PDF can no longer be used for online filing.

Nihang Law Insight

In practice, one of the safest habits is to diary the 180-day date the same day the certificate arrives, then create an internal “valuation checklist” for bank accounts, real estate, business interests, vehicles, and insurance. Most deadline problems start with delay in gathering values, not with the final form itself.

What Information Has to Go Into the Estate Information Return?

The return is an asset disclosure filing. Ontario requires identifying information about the deceased and a complete list of estate assets used to determine estate value, together with fair market value at the date of death. The estate trustee must report included assets carefully and avoid counting the same asset twice.

Figure 1: Asset Inclusion Decision Tree for the Ontario Estate Information Return

The Ministry guide says estate assets to be listed generally include Ontario real estate, bank accounts, investments, vehicles and vessels, and other assets, including goods, intangible property, business interests, and insurance proceeds if they pass through the estate. The guide also stresses that values are based on the date of death.

Some important exclusions appear in the guide as well. Property held in joint tenancy with a right of survivorship is generally not included, and assets passing outside the estate are generally not included. The guide also notes that only encumbrances on Ontario real estate are deducted in valuing that real estate; debts such as credit card balances or car loans generally do not reduce estate value for Estate Administration Tax purposes.

That is why valuation work matters. A later change in the real estate market does not usually change the required value, because the relevant valuation point is the date of death, not the sale date months later.

When Is An Amended Return Required?

An amended Estate Information Return may be required in several common situations: incorrect or incomplete information, refunds, additional tax payments, estimated values that later become final, or subsequently discovered property. In most of those scenarios, the amended return must be received within 60 calendar days of the triggering event.

Figure 2. Ontario Estate Information Return Filing and Amendment Timeline

The Ministry guide lays out the main amendment triggers. If an estate representative becomes aware, within four years of the certificate, that information already given is incorrect or incomplete, the amended return must be received within 60 calendar days of becoming aware of the issue. If the representative becomes aware after four years, the guide says there is no requirement to file an amended return for that reason.

If estimated values were used in the probate application and the court undertaking must later be fulfilled, the estate trustee may need at least two returns: the initial filing within 180 days, then an amended return within 60 days after the undertaking is fulfilled. If additional estate property is discovered after a certificate is issued, the Estates Act process may first require a statement to the court within six months of discovery, followed by an amended return within 60 days after that statement is delivered to the court.

| Situation | Deadline | Key point |

|---|---|---|

| Initial return after certificate | 180 calendar days | Applies even if no tax is payable on a sub-$50,000 estate with a certificate |

| Incorrect or incomplete information | 60 calendar days after awareness | Usually only if discovered within four years of issuance |

| Refund received | 60 calendar days after refund | Refund details must be reported |

| Additional deposit or tax paid | 60 calendar days after payment | Amended filing still required |

| Estimated value later finalized | 60 calendar days after fulfilling undertaking | Initial return still due within 180 days |

| Subsequently discovered property | 60 calendar days after court statement | Separate court step may be required first |

The table above reflects Ontario’s Ministry guide and the Estate Administration Tax / Estates Act framework.

Nihang Law Insight

The amendment rules matter most where estates contain private company shares, unusual personal property, or real estate that was not professionally appraised early. Those files often begin with reasonable estimates but later need better evidence. The risk is not the estimate itself; it is failing to amend once better information exists.

What Happens If You Miss the Deadline or Understate the Estate?

Missing the filing deadline can create real exposure. Ontario’s legislation permits audits, assessments, and reassessments, and it creates offence provisions for failing to comply with the filing requirement or making false or misleading statements. Late initial or amended returns may be assessed or reassessed at any time.

Figure 3: Reassessment Risk Following Late Filing, Non-Compliance, or Misrepresentation

The Estate Administration Tax Act says the Ministry may generally assess or reassess within four years after the tax became payable. But the Act also allows assessment or reassessment at any time where there was non-compliance with the information-giving requirement or a misrepresentation attributable to neglect, carelessness, wilful default, or fraud. The Ministry guide similarly states that a late initial or amended return can be assessed or reassessed at any time.

The offence section is serious. On conviction, a person who fails to comply with section 4.1, or who makes or helps make a false or misleading statement in the required information, may face a fine of at least $1,000 and up to twice the amount of tax payable by the estate, imprisonment for up to two years, or both. There is also a reasonable diligence protection for false or misleading statement offences.

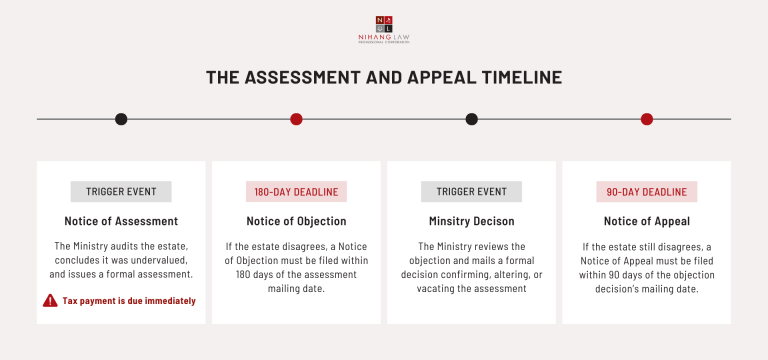

If the Ministry audits the return and concludes the estate was undervalued, it may issue a Notice of Assessment. The guide says payment is due immediately even if the estate trustee disagrees and plans to object. It also notes that no interest will be assessed on unpaid Estate Administration Tax, which is unusual enough that trustees should not assume ordinary tax rules apply in exactly the same way here.

If the estate disagrees with the assessment, Ontario’s guidance says a Notice of Objection must generally be filed within 180 days from the date the Notice of Assessment was mailed, and the broader Ontario tax appeals materials say a Notice of Appeal is generally due within 90 days from the mailing date of the Ministry’s decision on the objection.

A useful case-law note is Crichton v. HMTQ, 2021 ONSC 8012, where an Ontario court was described as emphasizing that the Estate Administration Tax regime is structured to channel tax disputes through the statutory assessment, objection, and appeal process, rather than inviting early court intervention by separate motion practice. That is one more reason to treat Ministry correspondence and objection deadlines seriously.

How Do You Calculate Estate Administration Tax, And Is It The Same As Income Tax After Death?

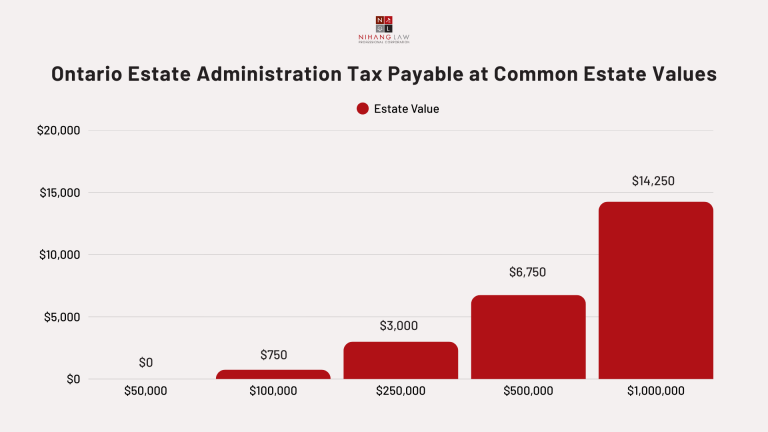

No. Estate Administration Tax is not the same as the deceased’s final income tax filings. In Ontario, the tax is generally $0 on the first $50,000 of estate value and $15 for every $1,000, or part of $1,000, above $50,000 when the estate certificate application is made on or after January 1, 2020. Separate CRA filing obligations can still arise on death.

Figure 4: Estate Administration Tax Payable at Common Estate Values in Ontario

For example, if the estate value reported for probate purposes is $250,000, the first $50,000 is exempt and the remaining $200,000 is taxed at $15 per $1,000, producing $3,000 in Estate Administration Tax. Ontario’s calculator and statutory wording reflect that structure.

That provincial tax issue is separate from federal and post-death tax filings. CRA explains that the deceased’s representative may need to file a final T1 return and, in some circumstances, additional returns such as T3 trust filings for post-death estate income. In other words, paying or calculating probate tax does not replace CRA compliance.

Ontario’s small estate process may simplify the court route for estates valued at $150,000 or less, but it does not eliminate the need to think carefully about tax and return obligations. Ontario’s probate guidance states that the simplified small-estate route is available up to $150,000, and official materials also indicate that an Estate Information Return still follows the issuance of the relevant certificate.

What is the Step-By-Step Roadmap for Estate Trustees?

The safest approach is to treat the Estate Information Return as a project that starts the day the certificate is issued. Confirm the certificate type, identify included assets, obtain date-of-death values, calculate tax, prepare the initial filing, and then monitor the file for later corrections or newly discovered assets.

Start by confirming exactly what certificate was issued and the issue date. Then list the assets that actually fall into the probated estate. Gather documentary support for date-of-death value, such as bank statements, appraisals, business valuation material, insurance records, and title or mortgage information.

Next, calculate the Estate Administration Tax deposit and prepare the initial return. If online filing is being used, confirm the Ministry’s current online process. If estimated values were used, note the undertaking and build a second deadline for the amended return. After filing, keep the supporting records organized at the estate representative’s principal place of business or residence in case the Ministry audits the file.

If new property is later discovered, or if earlier information turns out to be incomplete, do not wait for the estate year-end or for a property sale to sort it out. The statutory and guide-based timelines are event-driven, not convenience-driven.

What Mistakes Do Estate Trustees Make Most Often?

The most common mistakes are timing mistakes, valuation mistakes, and scope mistakes. Trustees often assume the 180-day deadline is flexible, confuse probate tax with CRA income tax, or fail to recognize that discovering new information can start a separate 60-day amendment deadline.

Common problems include:

waiting to gather valuations until close to the 180-day deadline;

using current market value instead of date-of-death value;

deducting debts that are not deductible for EAT purposes;

forgetting that estates under $50,000 may still require a return if a certificate was issued;

missing the amended-return deadline after finding an error or new property;

assuming a reassessment can only happen within four years even after late filing or non-compliance.

Nihang Law Insight

Many estate administration issues are fixable when raised early. They become expensive when the file has already been distributed, the property has been sold, or the trustee no longer has easy access to valuation records. A short review early in the file can prevent a much harder objection or reassessment fight later.

Frequently Asked Questions

Do I still need to file if the estate is worth $50,000 or less?

Yes, often you do. Ontario’s guide says a return is still required where an estate certificate was issued, even if the estate is $50,000 or less and no Estate Administration Tax is payable. The tax exemption and the filing obligation are not the same thing.

Does the 180-day deadline run from death or from probate?

It generally runs from the date the estate certificate is issued, not from the date of death. That distinction matters because there may be months between death, the probate application, and issuance of the certificate. Trustees should record the issue date immediately.

What if I used estimated values in the probate application?

That does not necessarily end the matter. Ontario’s guide says you may need an initial return within 180 days and then an amended return within 60 days after fulfilling the court undertaking once actual values are known.

What if I discover a new asset after the return was filed?

A separate court filing may be required first, and then an amended return may be required within 60 days after the statement is delivered to the court. The guide links this situation to subsection 32(2) of the Estates Act.

Can the Ministry still reassess the estate years later?

Yes, sometimes. Ontario’s Act generally allows assessment or reassessment within four years, but it also permits action at any time where there was non-compliance with the filing requirement or certain forms of misrepresentation. Late returns are especially risky.

What if the real estate market changed after death?

A later market change does not usually change the estate value for EAT purposes. The Ministry guide says assets are valued as of the date of death, so later market fluctuations generally do not require an amended return on that basis alone.

Can I file the Estate Information Return online?

Yes. Ontario’s official forms materials state that beginning March 3, 2025, the return can be filed online through the Ministry of Finance’s online services page, and the fillable PDF is no longer used for online filing.

Is Estate Administration Tax the same as inheritance tax?

No. Ontario’s probate tax is a provincial tax connected to the issuance of an estate certificate. It is different from the deceased’s income tax obligations, and Canada does not use a separate general “inheritance tax” in the way some other jurisdictions do. CRA death-year filing rules still need separate attention.

Key Takeaways and How Nihang Law Can Help

The practical takeaway is simple: the Estate Information Return deadline in Ontario is a real compliance deadline, not a formality. The 180-day filing rule, the 60-day amendment rules, and the Ministry’s audit and reassessment powers mean estate trustees should not wait until the estate is nearly wrapped up before turning to the return.

Where the estate includes real property, business interests, estimated values, newly discovered assets, or a missed filing date, early legal review may help reduce avoidable risk. Nihang Law can assist Ontario estate trustees with probate strategy, Estate Information Return compliance, amendment issues, and responding to Ministry assessments or objections. No result can be guaranteed, but careful planning and prompt action usually put the estate in a better position.

Sources & References

Estate Administration Tax: https://www.ontario.ca/page/estate-administration-tax

Calculating the Estate Administration Tax: https://www.ontario.ca/page/calculating-estate-administration-tax

Apply for probate of an estate: https://www.ontario.ca/page/apply-probate-estate

Probate of a small estate: https://www.ontario.ca/page/probate-small-estate

Administering estates: https://www.ontario.ca/page/administering-estates

Estate Administration Tax Act, 1998, S.O. 1998, c. 34, Sched.: https://www.ontario.ca/laws/statute/98e34

Estate Administration Tax Act, 1998, SO 1998, c 34, Sch | CanLII: https://www.canlii.org/en/on/laws/stat/so-1998-c-34-sch/latest/so-1998-c-34-sch.html

O. Reg. 310/14: Information Required Under Section 4.1 of the Act: https://www.ontario.ca/laws/regulation/140310

Estate Information Return – Forms – Central Forms Repository (CFR): https://forms.mgcs.gov.on.ca/en/dataset/9955

Guide – Estate Information Return – Estate Administration Tax Act, 1998: https://forms.mgcs.gov.on.ca/dataset/0b2647cd-52c1-4d3b-a7f0-7e2d3b3f01ca/resource/aae987c1-6a16-4dbf-a2d6-2871079adf40/download/9955e_guide.pdf

Objection and appeal procedures for Ontario taxes and programs: https://www.ontario.ca/document/ontarios-tax-system/objection-and-appeal-procedures-ontario-taxes-and-programs

Objections and appeals — Frequently asked questions, forms and publications: https://www.ontario.ca/document/ontarios-tax-system/objections-and-appeals-frequently-asked-questions-forms-and

What to expect during an Ontario Ministry of Finance audit: https://www.ontario.ca/document/ontarios-tax-system/what-expect-during-ontario-ministry-finance-audit

What returns you need to file – Prepare tax returns for someone who died – Canada.ca: https://www.canada.ca/en/revenue-agency/services/tax/individuals/life-events/doing-taxes-someone-died/prepare-returns/what-to-file.html

Thank you for reading this post, don't forget to subscribe!