16th March 2026BY Nihang Law

First-Time Home Buyer Rebates in Ontario: Who Qualifies and What You Can Actually Claim

Last Updated: March 2026

Ontario first-time buyers may qualify for more than one form of relief, but the programs do not all use the same eligibility test. A resale buyer usually looks first at the Ontario land transfer tax refund, and a Toronto buyer may also qualify for a separate municipal rebate. A federal home buyers’ tax credit may also apply, but it uses a four-year lookback rather than the stricter Ontario and Toronto “no prior ownership anywhere” rule. For certain new homes, the newer federal first-time home buyers’ GST/HST rebate may apply, and it can work alongside the existing Ontario new housing rebate.

Many Ontario buyers hear about a “first-time home buyer rebate” and assume there is one simple discount that appears automatically at closing. In practice, that is where people get into trouble.

Relief can arise in different ways depending on the measure involved. Certain benefits are claimed through land transfer tax, while others are claimed later on an income tax return. Some relief applies only to newly built or substantially renovated homes. In some cases, a spouse’s ownership history can disqualify the buyer even if the buyer personally never owned property. Federal measures may instead use a four-year lookback.

Missed deadlines, wrong assumptions about occupancy, or sloppy title planning can turn expected savings into a denial. The safest approach is to identify the exact program before closing, confirm who will be on title, and match the facts to the right eligibility test rather than relying on a generic “first-time buyer” label.

That review is ideally done before the deal is firm, while the Agreement of Purchase and Sale and any conditions can still be assessed properly.

Legal Disclaimer: This article is general legal information for Ontario readers and is not legal advice. Eligibility often turns on title structure, spouse history, occupancy, builder paperwork, and closing timing. Rules may change, and outcomes depend on the facts of the specific transaction.

Quick Start: Pick Your Path

Buying anywhere in Ontario on resale:

- Check the Ontario land transfer tax refund first.

Buying in Toronto:

- Check both the Ontario refund and the Toronto MLTT rebate.

Buying a new build or substantially renovated home:

- Also review the federal GST/HST rebate rules and the Ontario new housing rebate.

Filing taxes after purchase:

- Check the federal home buyers’ amount separately from closing rebates.

What Relief is Actually Available to First-Time Home Buyers in Ontario?

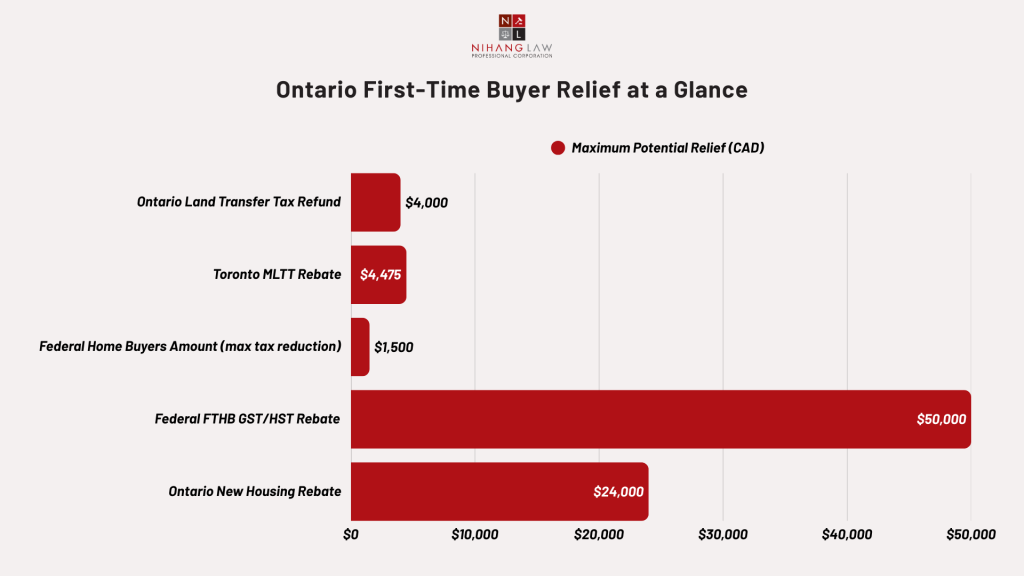

A first-time Ontario buyer may encounter four different types of relief: the Ontario land transfer tax refund, Toronto’s municipal land transfer tax rebate, the federal home buyers’ amount, and, for qualifying new homes, the federal first-time home buyers’ GST/HST rebate. These programs overlap, but they are not interchangeable.

The most important legal point is that “first-time home buyer” does not mean the same thing across all programs. Buyers who are also budgeting for closing costs should understand how land transfer tax is calculated in Ontario and Toronto, because the rebate analysis only makes sense in the context of the tax otherwise payable.

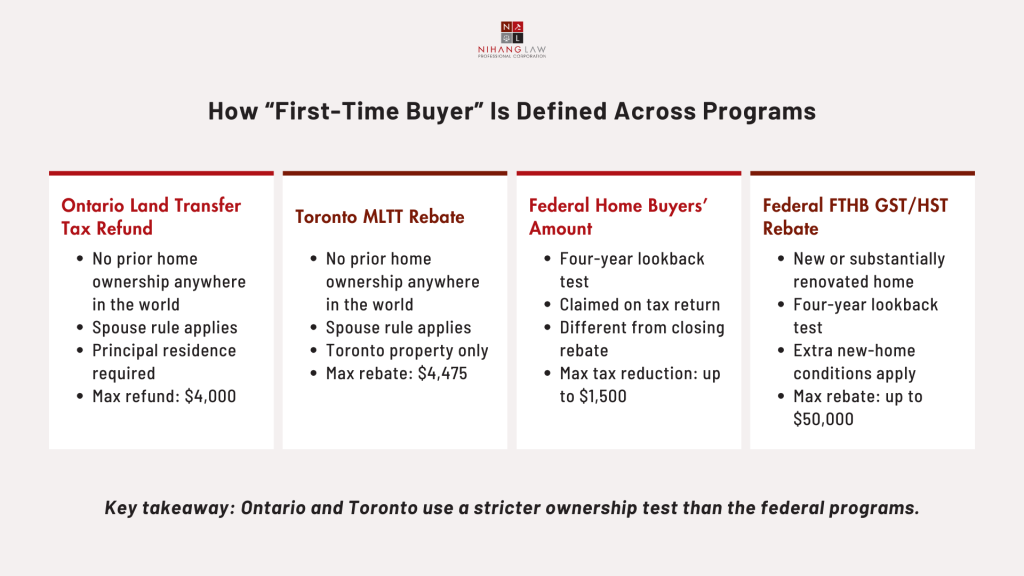

Ontario and Toronto use a stricter prior-ownership test tied to ownership anywhere in the world and the spouse rule. The federal home buyers’ amount and the federal GST/HST rebate generally use a current-year-plus-four-previous-years lookback.

Program | Typical transaction | Core test | Maximum relief |

Ontario land transfer tax refund | Resale or new home in Ontario | No prior ownership anywhere; spouse rule applies | Up to $4,000 |

Toronto MLTT rebate | Home in | Similar | Up to $4,475 |

Federal home buyers’ amount | Tax filing after purchase | No owned principal residence in acquisition year or prior four years, | Claim amount up to $10,000; tax reduction may be up to $1,500 |

Federal FTHB GST/HST rebate | Certain new | First-time | Up to $50,000 |

Ontario new housing rebate | Certain new or substantially renovated homes | Primary-residence new-housing rules; not limited to first-time buyers | Up to $24,000 |

The amounts and eligibility points above come from current official Ontario, Toronto, and CRA materials.

Figure 1: Ontario First-Time Buyer Relief At A Glance

Nihang Law Insight

In real closings, one of the most common mistakes is treating the federal tax credit as if it proves eligibility for Ontario land transfer tax relief. It does not. The tests are different, and that difference matters most where a spouse has prior ownership history.

Who Qualifies for the Ontario Land Transfer Tax Refund?

A buyer seeking the Ontario refund generally must be at least 18, must occupy the home as a principal residence within nine months, and must not previously have owned a home anywhere in the world. If the buyer has a spouse, the spouse’s ownership history can also matter.

Ontario’s materials state that the refund may be obtained at registration or by application to the Ministry of Finance within 18 months of the conveyance or disposition. Ontario’s guidance also confirms that the maximum first-time homebuyer refund is $4,000 for registrations on or after January 1, 2017.

The spouse rule is where many buyers are surprised. Ontario’s practitioner guide says a first-time purchaser is disqualified if their spouse owned a home while being that purchaser’s spouse. It also explains an important nuance: if the spouse sold that prior home before becoming the spouse of the purchaser, the refund may still be available.

Ontario also restricts this refund to Canadian citizens and permanent residents, with transitional relief where the purchaser becomes a citizen or permanent resident within 18 months of the transfer. That citizenship or permanent residence requirement is mirrored on Toronto’s municipal rebate page and reflected in Ontario’s official background materials.

Does Buying in Toronto Change the Analysis?

Yes. A Toronto buyer may face municipal land transfer tax in addition to Ontario land transfer tax, but a qualifying first-time purchaser may also claim a separate Toronto MLTT rebate of up to $4,475. That can be stacked with the provincial refund if both tests are met.

Toronto’s eligibility language is explicit. The purchaser must be at least 18, must occupy the home as their principal residence within nine months, must not have previously owned a home or any ownership interest anywhere in the world, and, if they have a spouse, the spouse cannot have owned a home anywhere in the world while they were spouses. Toronto also requires Canadian citizenship or permanent residence, but says a person who becomes a citizen or permanent resident within 18 months of the transfer may still apply and qualify.

If the rebate was not claimed at registration, Toronto says the buyer can apply afterward with supporting documents, including the transfer, agreement of purchase and sale, statement of adjustments, citizenship or permanent residence proof, and proof of occupancy. Toronto states that the completed application and supporting documents must be received within 18 months and that a processing fee applies.

Toronto buyers should also be aware that the City’s current MLTT page says new graduated rates for high-value residential properties take effect on April 1, 2026. That does not change the rebate test described above, but it may affect the underlying municipal tax payable depending on closing date and property value.

Nihang Law Insight

For Toronto files, the rebate analysis should be done before closing, not after. A buyer may qualify for both provincial and municipal relief, but the occupancy proof and title details should already be organized in case the claim is not fully handled on registration.

What Counts as First-Time for Federal Tax Relief?

For the federal home buyers’ amount, the test is generally whether the buyer did not live in another home in or outside Canada that they, or their spouse or common-law partner, owned in the year of acquisition or in any of the four preceding years. That is different from Ontario’s stricter prior-ownership rule.

CRA says the home buyers’ amount is a non-refundable federal tax credit that helps first-time buyers with some purchase costs. For the 2025 tax year, the claim amount is up to $10,000, and CRA guidance elsewhere explains that this can produce a tax credit of up to $1,500. Because it is non-refundable, it reduces federal tax otherwise payable but does not create a cash refund if no tax is payable.

CRA also says the buyer must intend to occupy the home as a principal place of residence no later than one year after acquisition. A disability exception applies where the disability tax credit requirements are met or the home is acquired for a related person with a disability and is better suited to that person’s needs.

This is often the cleanest example of why buyers should not collapse all programs into one. A purchaser may fail Ontario land transfer tax relief because of historic ownership or the spouse rule, yet still qualify for the federal home buyers’ amount because the relevant lookback is the acquisition year plus four prior calendar years.

Figure 2: How “First-Time Buyer” Is Defined Across Programs

When Does the Federal GST/HST Rebate on New Homes Apply?

The federal first-time home buyers’ GST/HST rebate applies only to certain new or substantially renovated homes, including some owner-built homes and some co-op situations. It is not the same as a resale closing rebate, and it depends heavily on agreement dates, construction timing, price, and first occupancy.

CRA’s current pages state that the rebate can recover up to 100% of the GST or federal part of the HST paid, up to $50,000, for new homes valued at or below $1 million. The maximum rebate is reduced between $1 million and $1.5 million, and there is no rebate at or above $1.5 million.

For homes purchased from a builder, CRA says the agreement of purchase and sale must have been entered into on or after March 20, 2025 and before 2031, construction or substantial renovation must begin before 2031 and be substantially completed before 2036, the buyer must be a first-time home buyer when ownership transfers, and the buyer must be the first individual to occupy the home as a residence after completion. CRA also says the program is not available to a corporation or partnership.

On process, CRA says that where the builder pays or credits the rebate, the builder must file the application. If the builder does not pay or credit it, the buyer generally has up to two years from transfer of ownership or possession, depending on the application type, to claim it directly. CRA’s current guidance also references Royal Assent on March 12, 2026 for certain transitional filing scenarios.

A separate but related point matters in Ontario: CRA’s existing Ontario new housing rebate remains available up to $24,000 for qualifying new housing in Ontario and is not limited to first-time buyers. Ontario’s 2025 fiscal materials discuss an additional Ontario first-time-buyer HST measure as a proposal tied to federal legislation, but buyers should not assume that proposed Ontario mirror relief is already available for their file unless the operative program and procedure are confirmed for the transaction date.

What Deadlines and Paperwork Usually Matter Most?

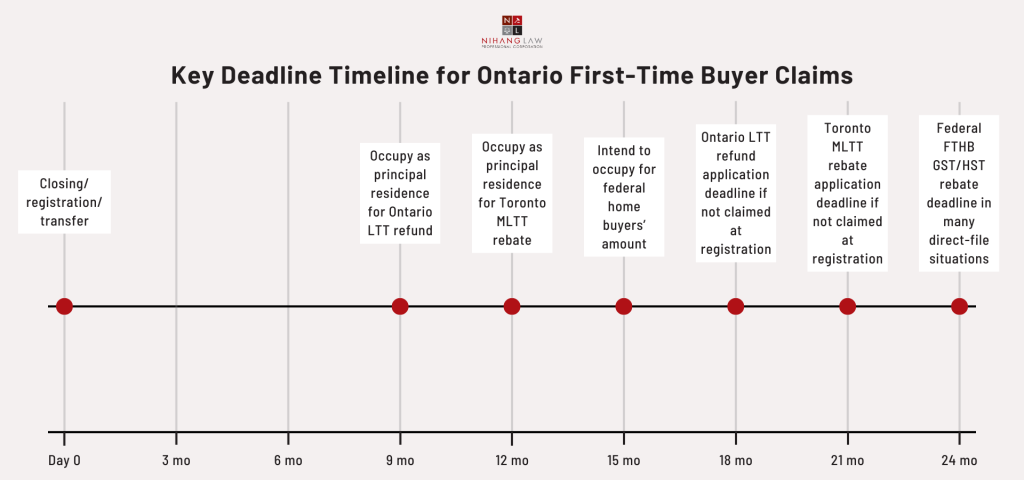

Most denials happen because the buyer used the wrong program, missed an application deadline, or could not prove occupancy and status. The practical answer is to match the file to the correct relief stream before closing and keep closing records organized for later claims.

For Ontario land transfer tax relief, the key timeline is principal residence occupancy within nine months and application within 18 months if the refund was not obtained on registration. For Toronto MLTT, the practical timelines are similar, and Toronto lists specific post-closing proof requirements. For the federal home buyers’ amount, the tax claim is made through the return, but CRA still expects supporting documents to be kept. For the federal FTHB GST/HST rebate, CRA says the filing route depends on whether the builder credits the rebate or the buyer files directly.

Figure 3: Key Deadline Timeline for Ontario First-Time Buyer Claims

Step-by-Step Roadmap

A buyer should first identify whether the property is in Toronto, whether it is resale or new, and who will be on title. Next, review prior ownership history for the buyer and spouse or common-law partner under the correct test for the specific program. Then confirm the principal-residence plan, gather citizenship or permanent residence documents where required, and decide whether any closing rebate is being credited at registration or must be claimed later. Finally, take note of the deadline and preserve the purchase agreement, statement of adjustments, registration records, and occupancy proof.

As part of that closing preparation, buyers should also understand title insurance and what risks it may or may not cover after closing.

What Mistakes Commonly Cost Buyers Money?

The most common mistakes are assuming all “first-time buyer” programs use the same rule, overlooking a spouse’s ownership history, missing the nine-month occupancy requirement for land transfer tax relief, missing 18-month or two-year claim windows, assuming a corporation can access personal housing rebates, and treating a proposed rebate as though it is already operational for the transaction.

Buyers looking for a broader practical checklist can also review these common mistakes first-time Ontario homebuyers make before closing.

Nihang Law Insight

Where family members are added to title for financing reasons, or where the buyer is newly landed and expects permanent residence status shortly after closing, the rebate analysis should be built into the conveyancing plan early. Small title or timing decisions can change eligibility.

Frequently Asked Questions

Can I claim the Ontario refund if my spouse owned a home before we met?

Often yes, but only if the spouse disposed of that home before becoming your spouse. Ontario’s guidance treats the spouse rule as a major eligibility issue and says the refund may still be available where the prior home was sold before the spousal relationship began.

Can I get both the Ontario and Toronto rebates?

Yes, if the property is in Toronto and you independently satisfy both the Ontario and Toronto first-time purchaser criteria. Toronto’s rebate is in addition to the provincial land transfer tax refund, not a substitute for it.

Is the federal homebuyer’s amount the same as a cash rebate at closing?

No. CRA describes it as a non-refundable tax credit claimed on the buyer’s tax return. It may reduce tax otherwise payable, but it is not the same as a closing adjustment or an automatic cheque from the closing lawyer.

Can I qualify federally even if I do not qualify in Ontario?

Yes, that can happen. Ontario land transfer tax relief uses a stricter prior-ownership and spouse rule, while the federal home buyers’ amount generally uses the acquisition year plus the previous four calendar years.

Does the federal GST/HST rebate apply to resale homes?

No. CRA’s current first-time home buyers’ GST/HST rebate is for newly built or substantially renovated homes, certain owner-built homes, and certain co-op situations. It is not a general resale-home rebate.

Can a corporation claim the federal first-time home buyers’ GST/HST rebate?

No. CRA states that the FTHB GST/HST rebate is not available to a corporation or partnership. The program is designed for eligible individuals meeting the first-time-buyer and primary-residence tests.

What if I did not claim the Toronto rebate on closing?

Toronto says you can apply afterward if you paid the tax at registration, but the application with all supporting documents must be received within 18 months and a processing fee applies.

Is Ontario’s new first-time buyer HST rebate already available?

Ontario’s published fiscal materials describe that measure as a proposal tied to federal legislative implementation. Buyers should confirm the live program rules for their closing rather than assuming the proposed Ontario mirror relief is already in force.

Key Takeaways and How Nihang Law Can Help

The main legal takeaway is simple: in Ontario, “first-time home buyer rebate” is not one rule. Provincial land transfer tax relief, Toronto’s municipal rebate, the federal home buyers’ amount, and the federal new-home GST/HST rebate all have different tests, deadlines, and evidence requirements. The biggest risk is using the wrong definition of first-time buyer or assuming a benefit applies automatically.

Nihang Law’s real estate team can help buyers and families review title structure before closing, flag spouse-history issues, confirm whether a Toronto file should be claiming both municipal and provincial relief, and identify whether a new-home purchase may involve GST/HST rebate planning in addition to ordinary conveyancing. That kind of review may prevent avoidable denials and post-closing disputes.

Reminder: Rebates and credits should be verified against the exact closing date, location of the property, title structure, builder paperwork, and the buyer’s personal and spousal ownership history before funds are released or a tax position is filed.

Sources and References

Ontario Ministry of Finance – A Guide for Real Estate Practitioners – Land Transfer Tax and the Registration of Conveyances of Land in Ontario: https://www.ontario.ca/document/land-transfer-tax/guide-real-estate-practitioners-land-transfer-tax-and-registration

Ontario Ministry of Finance – Land Transfer Tax Refunds for First-Time Homebuyers: https://www.ontario.ca/document/land-transfer-tax/land-transfer-tax-refunds-first-time-homebuyers

Ontario Ministry of Finance – Land Transfer Tax: https://www.ontario.ca/document/land-transfer-tax

Ontario Land Transfer Tax Act: https://www.ontario.ca/laws/statute/90l06

City of Toronto – Municipal Land Transfer Tax & Municipal Non-Resident Speculation Tax: https://www.toronto.ca/services-payments/property-taxes-utilities/municipal-land-transfer-tax-mltt/

City of Toronto – Municipal Land Transfer Tax & Municipal Non-Resident Speculation Tax Rebate Opportunities: https://www.toronto.ca/services-payments/property-taxes-utilities/municipal-land-transfer-tax-mltt/municipal-land-transfer-tax-mltt-rebate-opportunities/

Canada Revenue Agency – Line 31270: Home buyers’ amount: https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/about-your-tax-return/tax-return/completing-a-tax-return/deductions-credits-expenses/line-31270-home-buyers-amount.html

Canada Revenue Agency – First-time home buyers’ (FTHB) GST/HST rebate: https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/gst-hst-businesses/gst-hst-rebates/first-time-home-buyers-gst-hst-rebate.html

Canada Revenue Agency – What is the first-time home buyers’ rebate: https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/gst-hst-businesses/gst-hst-rebates/first-time-home-buyers-gst-hst-rebate/what-rebate.html

Canada Revenue Agency – Who can apply: https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/gst-hst-businesses/gst-hst-rebates/first-time-home-buyers-gst-hst-rebate/who-can-apply.html

Canada Revenue Agency – How to apply: https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/gst-hst-businesses/gst-hst-rebates/first-time-home-buyers-gst-hst-rebate/how-apply.html

Canada Revenue Agency – Applying for the rebate, home purchased from a builder: https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/gst-hst-businesses/gst-hst-rebates/first-time-home-buyers-gst-hst-rebate/how-apply/home-purchased-from-builder.html

Canada Revenue Agency – GST/HST new housing rebate: https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/gst-hst-businesses/gst-hst-rebates/new-housing-rebate.html

Ontario 2025 Fall Statement materials

Thank you for reading this post, don't forget to subscribe!